Virtual Data Rooms: M&A Trends and Industry Transaction History

This report is one in a series covering the market for virtual data rooms.

The average annual revenue growth observed in the Virtual Data Room (VDR) industry over the past 5 years is estimated at 7.9% by IBIS World[1], has attracted an increasing number of buyers interested in investing in industry players. While both the number and size of deals taking place in the industry in the past few years are still modest when compared to more established software-driven industries, such as cloud computing and e-commerce, a few notably large-sized deals have taken place in recent years.

Virtual Data Room Investment Overview

Between 2012 and 2017, a total of 52 disclosed deals have taken place in the VDR industry. The majority of these transactions involved M&A and private equity, and venture capital, which accounted for 19 and 27 of all deals, respectively. In 2017, only 5 transactions took place in the industry, totaling $1.12 billion in invested capital, and representing a 50% decrease in deal size when compared with the previous year, mainly pushed by a decrease in M&A and private equity. Furthermore, M&A and private equity deals have once again surpassed the number of venture capital deals, following a trend that began in 2016.

![]()

During the six-year period between 2012 and 2017, the total capital invested in the industry amounted to $3.97 billion. In fact, the capital invested in the last four years alone accounts for an astounding 97.66% of the almost $4 billion overall deal value for the entire period, despite the large drop in value observed in 2015.

![]()

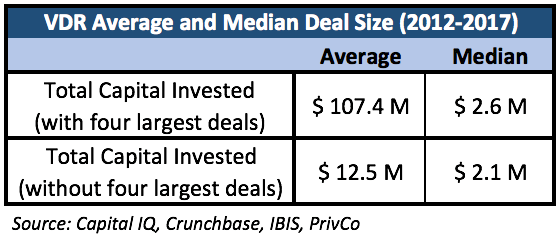

These numbers understate the overall amount of capital invested, since buyers and investors involved in 15 of those 52 M&A transactions have chosen to keep information concerning the specific funding amounts they provided to players in the industry private. Moreover, the substantial amounts of capital invested observed in 2014, 2015, and 2017 were mainly driven by four large transactions, which amounted to $3.56 billion, and can be somewhat misleading when evaluating the mean and median invested capital both for the entire six-year period and for each of the years from the period.

For example, the average deal size in the industry when including these four massive deals is 8.61 times larger than the average calculated in their absence during the entire period, calculated at $107.4 million and $12.5 million, respectively. As expected, the same trend is observed when calculating the annual average deal

size, with the unadjusted average deal size exceeding that of the adjusted by multiples of 11.95, 17.32, and 8.96, in 2014, 2016, and 2017, respectively. That being said, there is still a trend towards larger size deals, albeit not at the level suggested by the unadjusted calculations.

Major Buyers/Investors

Venture Capital Firms: high annual revenue growth in the past few years has attracted a considerable number of new players into the VDR industry. In fact, IBIS reports that 72 firms have joined the industry since 2012[2], and venture capitalists provided at least 27 of these firms with vital capital infusions.[3] This trend is expected to continue in the foreseeable future, as IBIS estimates that, on average, 20 new firms will join the industry annually in the five-year period leading to 2022[4], which might lead to a resurgence of venture capital deals.

Private Equity Firms: the fast pace at which annual revenues have grown in recent years, combined with an increase in industry profit margins[5], have led private equity firms to invest more often in the industry. In fact, four of the largest deals recorded in the industry involved private equity firms. These deals involved both the infusion of large amounts of capital in exchange for a minority ownership claim in industry players, such as in the case of HighQ Solutions. Outright acquisitions include deals like those inked by IntraLinks and Ipreo.

Industry Players: despite the consistent growth in the number of industry players, the VDR industry is still highly concentrated, with three large players earning 56.8% of all industry revenues[6], as of September 2017. Such concentration, together with the rapid pace with which players in the industry come up with improved platforms and solutions, creates incentives for market participants to acquire or invest in other firms. Thus, incumbent firms are motivated to acquire competitors as a way of either acquiring technologies they do not yet possess or increasing their market share by gaining access to clients held by the target firms, or both.

Notable Deals

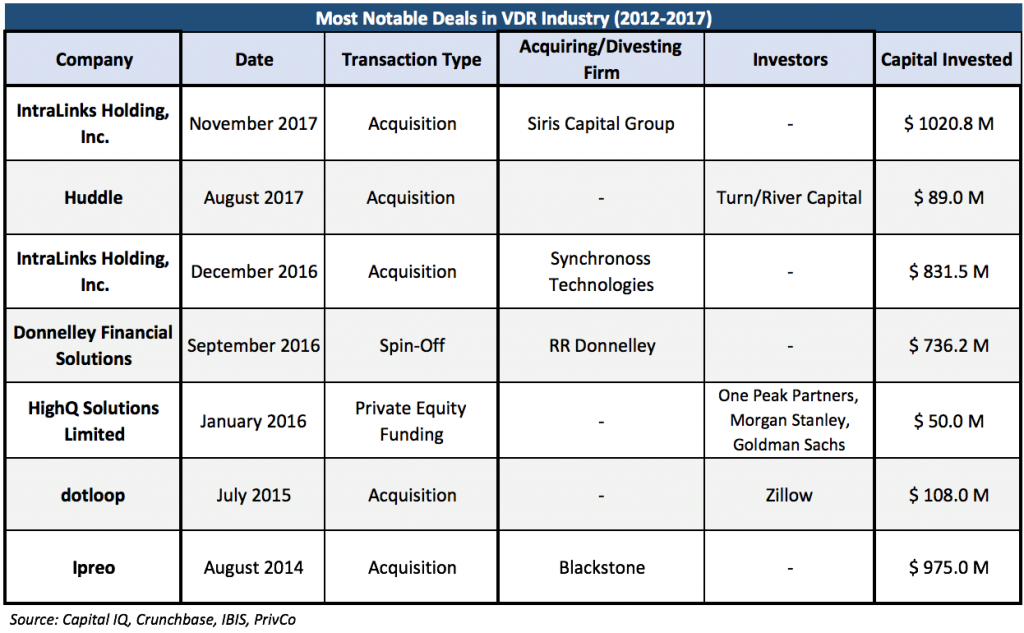

In the last four years, the VDR industry has seen its fair share of noteworthy deals. As merger and acquisitions volume soared, and the use of virtual data rooms with it, buyers turned their attention to some of the largest market players, as well as some of the smaller but fastest growing firms in the industry, hoping they would maintain their above average revenue growth, and therefore generate desirable rates of return on their investments. Most notably, IntraLinks, the market leader, was taken private by Synchronoss Technologies for $831.5 million in November 2016, and was acquired less than a year later by the private equity firm Siris Capital Group for $1.02 billion in consideration, which is thus far the largest transaction to have ever taken place in the industry. Other notable deals that involved private equity firms were the acquisitions of Ipreo by Blackstone in mid-2014, for an overwhelming $975 million, and most recently of Huddle by the tech focused firm Turn/River Capital, for $89 million[7], as well as the $50 million growth equity investment from One Peak Partners, Morgan Stanley Merchant Banking, and Goldman Sachs Private Capital in London-based HighQ Solutions.[8] On the other hand, the two remaining noteworthy deals were born out of business strategic motivations. In October 2016, Donnelley Financial Solutions, was spun-off by R.R. Donnelley, in an attempt to better position itself in the market[9]. It has since become the largest public VDR player, while managing to increase its market share from 11.7% to 14.0%[10], despite still falling behind Merrill Corporation and IntraLinks. Finally, dotloop was acquired by Zillow in 2015 for $108 million, as the online real estate database firm sought to enhance its value proposition by providing its customers with a more efficient solution to share and sign documents online.[11]

Sources

CapitalIQ, https://www.capitaliq.com/ (last visited Feb 5, 2018).

Crunchbase, https://www.crunchbase.com/ (last visited Feb 5, 2018).

Donnelley Financial Solutions Debuts as an Independent Company Following Spin-Off from R.R. Donnelley & Sons Company (2016), https://www.businesswire.com/news/home/20161003005457/en/Donnelley-Financial-Solutions-Debuts-Independent-Company-Spin-Off (last visited Feb 8, 2018)

Frederic Lardinois, Zillow Acquires DotLoop, An E-Signing Service For Real Estate Agents TechCrunch (2015), https://techcrunch.com/2015/07/22/zillow-acquires-dotloop-an-e-signing-service-for-real-estate-agents/ (last visited Feb 8, 2018).

HighQ completes $50 million growth financing round from One Peak Partners, Morgan Stanley Merchant Banking and Goldman Sachs Private Capital, HighQ, https://blog.highq.com/news/highq-completes-50-million-growth-financing-round (last visited Feb 8, 2018).

Iris Peter, IBISWorld Industry Report OD4593: Virtual Data Rooms in the US. IBISWorld (September 2017).

PrivCo, https://www.privco.com/ (last visited Feb 5, 2018).

Shona Ghosh, UK startup Huddle is being sold to a private equity firm for an estimated $89 million, Business Insider (2017), http://www.businessinsider.com/uk-startup-huddle-is-selling-to-turnriver-for-an-estimated-89-million-2017-8 (last visited Feb 8, 2018).

[1] IBISWorld Industry Report OD4593: Virtual Data Rooms in the US (September 2017)

[2] IBISWorld Industry Report OD4593: Virtual Data Rooms in the US (September 2017)

[3] https://www.capitaliq.com; https://www.crunchbase.com/; https://www.privco.com/

[4] IBISWorld Industry Report OD4593: Virtual Data Rooms in the US (September 2017)

[5] IBISWorld Industry Report OD4593: Virtual Data Rooms in the US (September 2017)

[6] IBISWorld Industry Report OD4593: Virtual Data Rooms in the US (September 2017)

[7] http://www.businessinsider.com/uk-startup-huddle-is-selling-to-turnriver-for-an-estimated-89-million-2017-8

[8] https://blog.highq.com/news/highq-completes-50-million-growth-financing-round

[9] https://www.businesswire.com/news/home/20161003005457/en/Donnelley-Financial-Solutions-Debuts-Independent-Company-Spin-Off

[10] IBISWorld Industry Report OD4593: Virtual Data Rooms in the US (September 2017)

[11] https://techcrunch.com/2015/07/22/zillow-acquires-dotloop-an-e-signing-service-for-real-estate-agents/

Marcelo Scott contributed to this report.

- Covid-19 Impact on US Private Capital Raising Activity in 2020 - May 27, 2021

- Healthcare 2021: Trends, M&A & Valuations - May 19, 2021

- 2021 Outlook on Media & Telecom M&A Transactions - May 12, 2021