Pros and Cons of Employee Stock Ownership Plans (ESOPs)

An employee stock ownership plan (ESOP) are utilized by private equity (PE) firms and business owners as an alternative exit strategy to structure a business sale or acquisition. PE firms collaborate with ESOPs to secure investments and use it as a form of exit strategy for current portfolio companies. Majority owners can also use ESOPs as a means to transition ownership in a management buyout.

The article will present an overview of ESOPs including the purposes, characteristics, structures as well as the benefits and disadvantages of structuring an ESOP.

Overview

ESOPs are tax-qualified retirement plans subject to the Employee Retirement Income Security Act of 1974 (ERISA) and are used in transactions for acquisitions. In a transaction, ESOPs can be used to buy shares and to acquire 100% of a company’s stock in one transaction. The main aspect of the ESOP is that it must be invested in employer stock.

Purposes

- Utilized in the succession organizing of a company’s ownership by purchasing retiring shareholder shares. Generally, ESOP’s share purchases are tax-deductible or tax-incentive dollars.

- Used to purchase subsidiaries or divest, to repurchase outstanding shares, or to reconstruct an existing benefit plan by substituting existing plans with an ESOP.

- Used to purchase recently released shares in the sponsoring company. In a leveraged situation, the sponsoring company, funds acquisition or growth with tax-deductible debt repayments.[1]

Criteria for Successful ESOP Structure

- Highly educated and well compensated workforce. This criteria is significant since employees are provided with incentives to think like an owner, especially in instances when an ESOP is used to transition out certain existing owners.

- Relatively stable cash flow and expertise in management team. The cash flow is used to support the borrowed funds.[2]

Characteristics of a Good ESOP Candidate

- Private business owners who desire to offer their stock for full fair market value and at the same time maintain the management of the company.

- Companies (typically private equity groups) that want to decrease the cost of acquisitions and/or outbid rival companies in a competitive M&A bid situation.

- Companies that plan to remove principal payments on current or new loans to fund growth.[3]

Structure

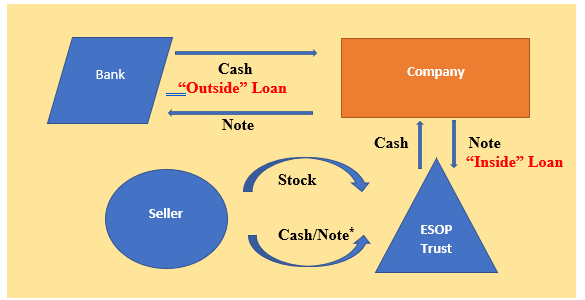

Leveraged ESOP Transaction

The company uses the balance sheet to borrow funds from a senior lender. The borrowed funds are termed the “outside loan".[4] The seller shareholders will also often fund the balance of the equity portion of the total purchase price. Private equity group notes and warrants are also frequently to finance the transaction. The proceeds from the senior and subordinated debt are loaned to the ESOP, (the “inside loan”), enabling the ESOP to buy all the common stock of the target company.Basic Structure of a Leveraged ESOP Transaction

Source: Americanbar.org

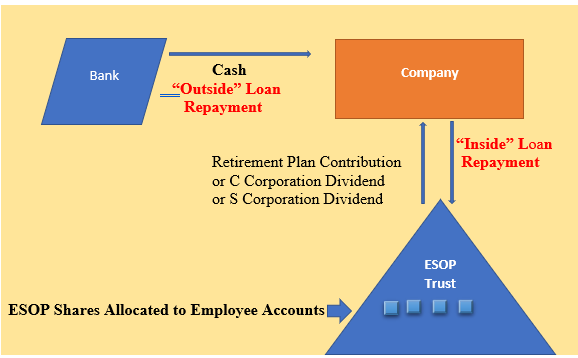

Post- Leveraged ESOP Transaction

Subsequent to an ESOP transaction, the company must annually make tax-deductible contribution to the ESOP to refund the inside loan. The ESOP trustee uses the funds to make payments to the company on the inside loan. In addition to the contributions, the company can announce and release tax-deductible dividends (C corporation) or dividends distributions (S corporation) on shares of the corporation’s stock managed by the ESOP.

Principal and interest payment on the inside loan are made by the ESOP trustee and employees who engage in the ESOP to obtain shares of the corporation’s stock.4Basic Structure of a Post-Leveraged-Transaction Cash Flow

Source: Americanbar.org

Benefits

- The seller of the business gains from an ESOP transaction due to an increase in after-tax proceeds. For example, the business owner can exclude or indeterminately defer capital gains taxes pursuant to the sale of the business.

- The financial strength and operations of the business are enhanced from corporate tax savings, employee motivation and cash flow are also improved.

- The PE firm and senior creditor benefit from the ESOP transaction since the investment produces a reduced risk profile based on multiples of effective EBITDA.

- The ESOP structure provides liquidity to the company and to equity holders.2

- The structure of the ESOP enables business owners to customize and merge their business exit. Business owners can plan their personal retirement as they sell some shares to gain some liquidity.

- The structure of the ESOP helps the owner of the business to establish control of the business and to gain personal diversification as well as potential upside.

- ESOPs can be effective retention tools. Employees can be retained due to the retirement benefits produced by the ESOP.

- Shareholders can sell part or all their stock since ESOPs create a market for shareholders. Additionally, ESOPs can pay up to full fair market value stocks sold by shareholders.

- Shareholders can also diversify their wealth. ESOPs provide shareholders with the flexibility to establish a proportion of wealth to diversify.3 Shareholders can decide what portion of their stockholdings they can sell to ESOPs.

Disadvantages

- Corporate governance — the transaction can be placed at risk when ESOP trustees and external advisers develop impatience with the sale-process time line due to potential delays inherent in the setup time required.

- There is the potential for dilution in the deal’s value when ESOP trustees utilize their rights of approval to obtain a premium for their stock.

- The company may experience a cash flow drain since cash flow contributed to the ESOP can limit the availability of the cash to reinvest in the business.[5]

- ESOPs may require employees to make financial sacrifices including wages and benefit rollbacks. Although, employees may agree to such agreements, it may not appeal to them.

- There is additional cost to the company that includes retaining an independent trustee, legal counsel and financial advisor as well as the legal expenses associated with an ESOP.[6]

Conclusion

ESOPs are sometimes used as an alternative strategy to structure a company sale. ESOPs are typically used to buy subsidiaries, divest, and/or acquire recently released corporate shares. The characteristic of a company determines the viability of structuring an ESOP. In a leveraged transaction, the company borrows funds from senior lenders to finance the transaction and the proceeds from the loan are used to buy the stock of the company, whereas in a post-leveraged transaction, the ESOP trustee uses funds to make payments to the inside loan.

Companies, their shareholders, management and private equity groups have all used ESOPs to their benefit. However, the additional incurred costs associated with the ESOP as well as the potential risks with the transaction raises concerns over the suitability of an ESOP structure for every deal.Sources[*] Seller Financing often used[1] JAMES R. HITCHNER, FINANCIAL VALUATION: APPLICATIONS AND MODELS, (2017).[2] Matthew J.

Hickro & Ira Starr, Private Equity and ESOPs: A Creative Combination, https://www.longpointcapital.com/site/assets/files/1220/private-equity-and-esops-a-creative-combination.pdf.[3] Dickinson Wright, What is an ESOP, (2013), http://www.dickinson-wright.com/-/media/files/publications/2013/03/what-is-an-esop.pdf?la=en.[4] Sharon B. Hearn, ESOPs: A Tax Advantaged Exit Strategy for Business Owners, (2015), https://www.americanbar.org/publications/blt/2015/03/02_hearn.html[5]George D.

Shaw ,The Pros and Cons of ESOPs, (Jan 28, 2013), http://ww2.cfo.com/tax/2013/01/the-pros-and-cons-of-esops/.[6] Gary Miller, Advantages and Disadvantages of an ESOP, (July 5, 2016), https://www.axial.net/forum/advantages-disadvantages-esop/.Jenn Abban contributed to this report.

Considering a transaction?

Speak with our advisory team about your sell-side, buy-side, or capital needs — in confidence.