.png)

Surety bonds are regularly utilized to support the acquisition goals for independent sponsors and private equity (PE) groups alike. In recent years, PE firms have invested in construction industries and have used surety bonds to assure contractor payments. The article will present an overview of surety bonds including the characteristics of the bond as well as bond termination, penalty, options to terminate certain types of bonds and four types of surety bonds. The article will also include a discussion of the criteria required by surety companies as well as the advantages and disadvantages of utilizing surety bonds to raise capital.

Overview

A surety bond is essentially an agreement between three parties and includes the principal, the surety and the obligee. Surety bonds are typically used to safeguard against contracts from future insecurity and risk. The surety is the party responsible for the contract, obligation or debt. Typically, the surety is a surety bond broker or insurance company. The purpose of the surety is to answer for the default on the principal�s behalf in accordance to the provisions set forth in the bond agreement.[1] In PE transactions, the principal is the PE firm, whereas, the obligee, is the contracting firm.

Characteristics of a Surety Bond

- The principal is the party that the obligee requires to take out the surety bond. The surety bond protects the obligee from violations of contracts or unethical business practices.

- The obligee is the party that expects a surety bond as a form of protection. Obligees are either individuals, companies or government agencies that utilize the surety bonds to conceal damages during a claim.

- The principal posts collateral with the surety, typically, up to 100% of the bonded amount.

- The principal is expected to endorse an indemnity agreement to support the surety.

- The principal and surety agree to pay the obligee a specific amount for damages if the principal defaults. [2]

- Prior to any declaration, there must be a meeting among the principal, the obligee and the surety to discuss any existing problems.1

Bond Termination

- Bond expires when the debt is completed.

- Some bonds may be in effect for an undetermined time.

- Non-cancelable bonds expire only when the agreement is met.

Bond Penalty

- Liability limit placed on the bond.

- In the event of a loss, the penalty is the maximum amount that the obligee must pay.

Surety Bond Premium

- The specific money paid to a surety company to ensure that a surety bond guarantee is provided.

- Premium, the rate, is usually one to two percent of the face value of the bond.2

Surety Rights of Indemnity

- The surety company requires the principal to execute an indemnity agreement to support the surety.

- In cases where the surety company pays a claim under the surety agreement, the surety company has the right to request for reimbursement or indemnification from the principal.

Options to Terminate Contract During a Default

The tender option � The obligee and surety can consent on a replacement contractor to complete the bonded work. The surety tenders a new contractor to the obligee. Subsequently, the obligee has the advantage to deal directly with the new contractor.Takeover option � The surety itself assumes the responsibilities of the work to complete it. Furthermore, the surety appoints professionals to oversee the work.Advise the obligee � The obligee is informed that the surety opts to not be involved in the work. This option prevents unduly delays from completing the work.1

Four Types of Surety Bonds

Contract surety bond � Guarantees the performance of a bonded contractor. This type of bond is the most common type of bond, and the bond ensures that a contractor adheres to the designs of a construction contract. The project owner is the obligee and the surety bond guarantees that the principal contractor will accomplish the contract.Commercial surety bond � Pledges performance in circumstances that occur from other contracts. The obligee to this type of surety bond is public. Typically, government agencies mandate that new businesses obtain a commercial surety bond.Fidelity surety bond � This type of bond protects the firm against the negligence of an employee who manages cash to warrant against financial losses as well as the customer�s money, personal materials and equipment.Court surety bond � The bond is demanded by an attorney prior to a court proceeding as a security against potential losses. In addition, this type of bond typically pledges the costs of payments associated with the lawyer�s fees.1

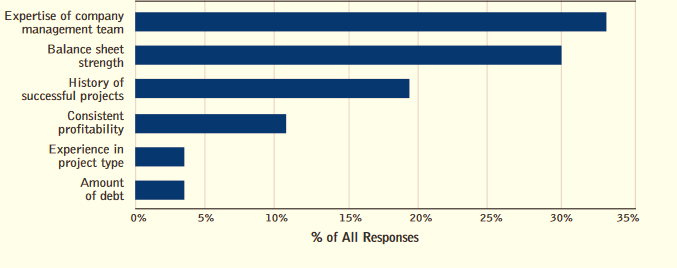

Criteria to Provide Surety Credit to PE Firms

- Surety companies need assurance about the status of PE companies.

- Companies must have historical success to serve as the principal for surety bonds.

- Strong management team with expertise as well as management with a continuity plan.

- Companies must maintain positive working capital and substantial equity.

- The strength of the balance sheet is significant since it determines the ability of the PE firm to service debt.[3]

- Due to the large debt in PE transactions, surety companies demand more security and require firms to have available funds to reimburse contractors in a claim scenario.[4]

- Surety companies also require higher net worth restrictions on the debt amount in the indemnification and transaction.3

Surety Executive Survey

Source: FMI Corporation

Benefits

- Surety bonds support industry standards by offering customers a trustworthy way to make a demand against companies that provide low standard goods and services.

- The surety bond assures that the work will be completed based on the contract. Additionally, selecting a tender option during a default, also shifts the risk of completion of the project to the surety for the contractor to complete the project.

- The takeover option is also beneficial to the surety since the costs of completing the project is controlled by the surety company during a default.[5]

- Surety professionals have expertise in addressing troubled projects and the expertise of surety professionals can help prevent a default termination.1

Disadvantages

- PE firms are unwilling to offer indemnity to the surety company since PE deals lack parental indemnity. Additional risk is incurred as assets are upstreamed to the parent company that does not provide indemnity.[6]

- The cost of completing the contracted project can increase when a tender option is selected.

- The risk of the surety is unknown when a takeover option is selected during a default.

Conclusion

Surety bonds support to the increase in contracting opportunities and are frequently used in the construction industry. Private equity companies represent the principal, whereas the obligee is typically a contracting company from another industry. The surety company utilizes the surety bond as a guarantee against unforeseen financial challenges that may arise with the principal. During a default case, the surety company has the option to takeover, tender a new contract or advise the obligee. Surety companies ensure that PE firms meet certain criteria prior to structuring surety bonds to support their business plan. Although, the surety company and obligee benefit from surety bonds, additional risks can be incurred when PE firms are unwilling to provide indemnity.Sources[1] The Associated General Contractors of America, An Overview of the Contract Surety Bond Claims Process, (2004), https://www.suretec.com/uploads/files/AGC%20surety%20claims%20guide.pdf.[2] Evan Tarver, Surety Bonds & How They Work, (Aug 17, 2017), https://fitsmallbusiness.com/what-is-a-surety-bond/.[3] Timothy R. Sznewajs & Curt M. Young, Surety Firms Weigh in on Construction Markets and Contractors:FMI Surety Providers Survey, (2010), https://www.asaonline.com/eweb/upload/SuretySurvey_2010April.pdf.[4] http://www.lockton.com/whitepapers/Fuchs_Revival_of_Private_Equity_Deal_Placement_Dec14.pdf[5] R. James Reynold, Jr, Handling Surety Performance Bond and Payment Bond Claims, MARGOLIS EDELSTEIN, http://www.margolisedelstein.com/files/reynolds_-_surety_performance_bond_claims_1.pdf.[6]Jeff Ciecko, Don�t Let Surety Be an Afterthought When Acquiring a New Construction Company, (Oct 19, 2016), http://enewsletters.constructionexec.com/riskmanagement/2016/10/dont-let-surety-be-an-afterthought-when-acquiring-a-new-construction-company/.Jenn Abban contributed to this report.

.png.png)