.png)

The semiconductor industry includes products such as memory chips, microprocessors, integrated circuits, and specialized System on a Chip (SoC) processors. These product categories serve a wide variety of end uses in all types of electronics and computers. �The first three categories are dominated by large companies with thin margins, while the fourth category is more accessible to smaller, niche players1.Annual revenue growth for the semiconductor industry this year is expected to reach 11.5%. This is the highest growth the industry has seen since 2010, and it is driven heavily by growth in newer markets2. Growth in the larger markets, such as integrated circuits, has slowed in recent years mostly due to declining PC sales3. Because of this and the intense level of competition manufacturers now face, the industry is ripe for consolidation.

Industry Profile

Multiple product categories of semiconductors, such as microchips and memory, are used in manufacturing computer motherboards.

Source: WSTS End Use Report

The semiconductor industry is marked primarily by large companies that can afford the continuous capital expenditures and R&D costs necessary to stay current in an evolving industry. In 1965, Gordon Moore of Intel predicted that the number of transistors per square inch would double approximately every two years. This principle, known as Moore�s Law, has become the standard for the industry1. Because of this, semiconductor companies spend more on R&D as a percent of revenue than any other industry4. Modern semiconductor manufacturing is an extremely complex and involved process that requires expensive machinery costing billions of dollars3. This complexity can be seen by looking at the evolution of microprocessors since the 1980s. In 1985, semiconductors were built on a two-dimensional surface and only used 11 of the elements on the periodic table as inputs. Today, semiconductors are three-dimensional and use more than 50 elements5. Small businesses find it hard to keep pace with the costs and complexities associated with manufacturing semiconductors, so large players have come to dominate a significant portion of the industry1.Other notable features of the semiconductor industry include its cyclicality, high lead times, and steep competition. The industry is marked by boom and bust cycles. These occur because when prices for products are high, companies produce more, which leads to market saturation and a drop in prices. In turn, this causes companies to produce less and prices gradually rise back up6.The industry�s high lead times stem from the amount of effort required to design, develop, and manufacture the next generation of semiconductor products. It can take years for a concept to see actual production. This means that companies must be able to estimate trends years in advance, which can be difficult7.

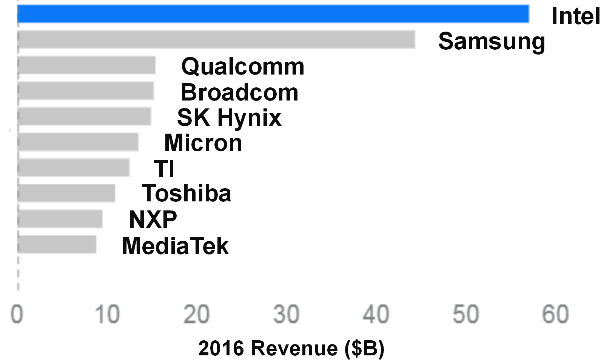

Intel is the world's largest semiconductor company by revenue. Source: IC Insights Database

The industry also faces steep competition, both in the design and in the manufacturing of chips. Companies invest heavily to stay ahead of one another in terms of product specifications and efficiency. Leading-edge fab is getting increasingly more expensive to implement and as time passes, fewer and fewer companies have the cash flows to sustain the continued investment costs7. A good example of this is memory chip manufacturers. In 2003, there were over 40 scaled producers of memory chips. Ten years later, less than 10% remained3.

Trends

Decline in PC SalesThe popularity of mobile devices, including tablets and smartphones, have taken a toll on the traditional market for PC sales, which includes desktops and laptops. Analyst estimates suggest that PC shipments declined in the third quarter of 2017 between .5 to 3% below their levels during the prior year8. This affects large microprocessor companies such as Intel. Both major industry analysts, IDC and Gartner, suggest that this is a long-term downtrend and not just a downturn in the sales cycle9.MobileProducers of semiconductors for mobile devices, on the other hand, are seeing strong growth. Intel did not position itself in time to capture this trend fully, but companies such as Samsung, Qualcomm, TSMC, and Texas Instruments stand to benefit from it. Apple stands to gain as well, not because it produces the microprocessors used in its own phones, but because it designs them10. To compare the significance of �mobile to PCs, last year a total of 1.5 billion smartphones were sold, as compared to 175 million tablets, 157 million laptops, and 103 million desktops11,12.Servers and Data CentersAnother semiconductor trend is the recent importance of servers and data centers in the era of big data. Businesses have more data than ever, and they need places to store and process it. To meet this need, companies such as Amazon, Google, Microsoft, and IBM are investing heavily in cloud infrastructure and hosting, leading to high volumes of servers being produced13. Intel and NVIDIA are the semiconductor companies positioned strongly here, with Intel leading on the server side and NVIDIA leading on the data processing side. NVIDIA historically was known as a manufacturer of graphics cards for PCs, but the trend to process big data with graphics processing units (GPUs) has benefited it enormously. The reason behind this trend is that although GPUs have smaller cores, there are a lot more of them, so they are more efficient at handling repetitive calculations13.

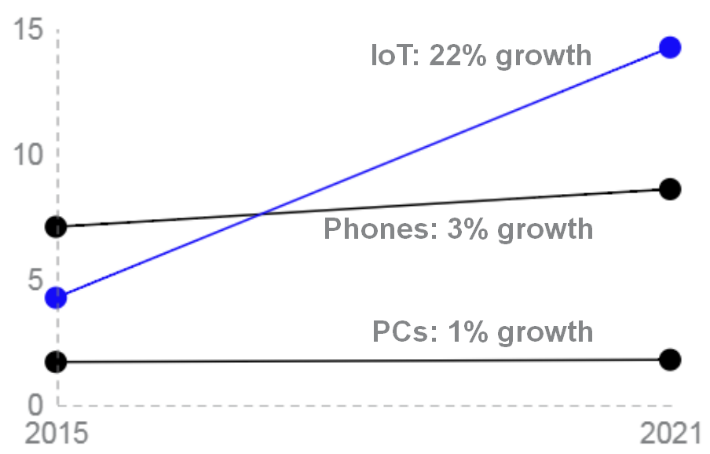

Internet of Things (IoT)

Source: Ericsson Mobility Report

The Internet of Things space includes segments such as automobiles, homes, retail, and factory, which are all becoming technology enabled. This trend is largely still in its early stages, but is poised for rapid growth within the next 5 to 10 years. McKinsey estimates that the total addressable IoT market will be over $350 billion by 20154. Because of the opportunity for growth and the chance to capitalize on specific niches, this space currently has lots of players vying to capture the market. It is also seeing acquisitions from large companies looking to position themselves to capitalize on the future growth opportunities.

Transactions

Mergers and acquisitions in the semiconductor space�have included�some high-profile mega deals because of margin pressure, competition, and slower growth in the PC industry. What follows are a handful of the major deals that have occurred recently and the rationale behind them. The transactions are broken down into two major categories: consolidation transactions and acquisitions in new markets.Consolidation TransactionsBroadcom/Qualcomm - 2017Broadcom made an unsolicited bid for Qualcomm for $105 billion in early November of 2017. Qualcomm ultimately rejected the offer, but Broadcom says it is still committed to the deal and intends to implement strategies to win over management and shareholders. If successful, the purchase would mark the biggest technology takeover to date. Both Broadcom and Qualcomm are sizable chipmakers and the transaction reflects Broadcom�s belief that it would benefit from increased economies of scale14.Qualcomm/NXP - 2016In October of 2016, Qualcomm announced that it agreed to pay $39 billion to acquire NXP, a manufacturer of semiconductors and the largest producer of automobile chips15. This shows both vertical integration and consolidation and how companies in slower-growing markets have sought to position themselves for coming trends. The deal has not yet closed, but is set to do so early in 2018.Other notable, though less recent consolidation transactions include:

- Analog Devices� acquisition of Linear Technology for $14.8 billion - July 201616

- Western Digital�s acquisition of SanDisk for $19 billion � Oct 201517

- Avago�s acquisition of Broadcom for $36.6 billion � May 201517

New Market TransactionsIntel/MobileyeIn March of 2017, Intel announced that it would acquire Israeli chip designer Mobileye for $15.3 billion. Mobileye specializes in technology for autonomous vehicles, and the acquisition positions Intel to be a leader in the business of computer-assisted driving. Referring to the acquisition, Intel�s CEO described an autonomous car as a �server on wheels.� Intel largely missed the mobile boom in chip technology, so they hope that the car market will position them for future growth18.Softbank/ARM HoldingsSoftbank�s foray into the Internet of Things space with the acquisition of ARM Holdings was announced in July of 2016. Softbank, a Japanese internet and telecommunications conglomerate, is looking for opportunities in faster-growing markets, and the deal represents Softbank�s bet on the trend towards mobile and networking19.Intel/AlteraIntel announced it would acquire Altera for $16.7 billion in June of 2015. The transaction is Intel�s largest to date and allows it to directly enter the networking and wireless applications markets. Additionally, the transaction will provide Intel with technologies to capture market share in the growing Internet of Things space20.

Opportunities

Current opportunities in the semiconductor space are mainly concentrated in the younger markets that are less consolidated and positioned for rapid growth. Today, System on a Chip (SoC) companies have an opportunity to build out a specialization within a market. This is what Mobileye did by building circuits specifically designed to be implemented into autonomous vehicles. The automotive-semiconductor market currently generates sales of over $30 billion annually and is expected to reach $40 billion in sales by 20204.Other examples of niche opportunities include office building sensors and the semiconductor security space. The technology is still in its early stages, but eventually office buildings will be connected by sensors and circuits that allow monitoring of temperature, power usage, cameras, and door locks. One reason there is a market for this technology is that building management companies can save money by maintaining better controls over their facilities. Additionally, occupants are willing to pay a premium to have greater control and flexibility4.As for the semiconductor security space, more and more connected devices and servers brings a greater need for system security. A smart alarm system that protects a building will not be very advantageous if a hacker knows how to crack the chip in the alarm. Companies that can develop technology to address these growing needs in an ever-connected word stand to benefit enormously4.

Threats

One threat to the semiconductor industry is the rise of what are called �fabless� chip makers. Being �fabless� means that a company does not own manufacturing equipment, but instead competes on the design and intellectual property used in making the microprocessors1. An example of this is Apple, who surprised its semiconductor suppliers by announcing that it would design its own chips21. The rise of fabless companies has resulted in a shift of power from traditional semiconductor companies to new entrants.A second threat to the semiconductor industry is the protection of intellectual property. This includes protecting designs from competitors who can reverse engineer them and protecting the legal rights to a patent. Companies that spend billions of dollars on research and development try to recoup the costs in the pricing of their components. However, they face the problem that competitors can reverse engineer the hardware, copy the technology, and then sell it at a lower cost because they do not have R&D expenses to recoup1. Additionally, protecting the legal rights to use intellectual property can be difficult. A current, high-profile example of the dispute between is Qualcomm and Apple. Qualcomm argues that Apple infringed on their patents while Apple states that Qualcomm is licensing its technology illegally22.One last threat that needs to be mentioned�though it affects potential for strategic M&A more than the industry itself�is that recent semiconductor acquisitions by foreigners have come under scrutiny by various governments. This is because policy makers have come to see semiconductor technology as an issue of national security due to the disruption a cyberattack by a foreign entity could have. A high-profile example of this is when President Trump blocked the acquisition of Lattice Semiconductor by a group of investors tied to China23.

Conclusion

There is no doubt that significant changes are in store for semiconductor companies in the years ahead. New technologies will emerge, and competition will remain fierce. Trends towards IoT, mobility, and networking will change the future of the industry. Due to these factors, it is probable that M&A activity will remain heated in the years to come.Citations

- Investopedia Staff, The Industry Handbook: The Semiconductor Industry Investopedia (2017), http://www.investopedia.com/features/industryhandbook/semiconductor.asp (last visited Nov 14, 2017).

- Dan Rosso, Global Semiconductor Sales Increase 21 Percent Year-to-Year in April; Double-Digit Annual Growth Projected for 2017 Semiconductor Industry Association (2017), https://www.semiconductors.org/news/2017/06/06/global_sales_report_2017/global_semiconductor_sales_increase_21_percent_year_to_year_in_april_double_digit_annual_growth_projected_for_2017/ (last visited Nov 14, 2017).

- Best of Semiconductor Market View, Semi.org (2015), http://www.semi.org/eu/sites/semi.org/files/data15/docs/03_Heinz Kundert_SEMI.pdf (last visited Nov 18, 2017).

- McKinsey on Semiconductors Issue 6 2017, McKinsey & Company (2017), https://www.mckinsey.com/~/media/McKinsey/Industries/Semiconductors/Our%20Insights/McKinsey%20on%20Semiconductors%20Issue%206%20-%20Spring%202017/McK%20on%20Semiconductors_Issue%206_2017.ashx (last visited Nov 18, 2017).

- Materials Innovations Move Moore and More Chips, Semi.org (2016), http://www.semi.org/en/node/55021 (last visited Nov 18, 2017)

- Jim Handy, The 3 Reasons Semiconductor Experience Revenue Cycles Forbes (2014), https://www.forbes.com/sites/jimhandy/2014/05/28/the-3-reasons-semiconductor-experience-revenue-cycles/#67cbae465386 (last visited Nov 14, 2017).

- McKinsey on Semiconductors, McKinsey & Company (2011), https://www.mckinsey.com/~/media/mckinsey/dotcom/client_service/semiconductors/pdfs/mosc_1_revised.ashx (last visited Nov 15, 2017).

- Emil Protalinski, Gartner: Global PC shipments fell 3.6% in Q3 2017, 12th straight quarter of decline VentureBeat (2017), https://venturebeat.com/2017/10/10/gartner-global-pc-shipments-fell-3-6-in-q3-2017-12th-straight-quarter-of-decline (last visited Nov 15, 2017).

- Simon Sharwood, Gartner says back-to-school PC sales failed. IDC says they worked The Register (2017), https://www.theregister.co.uk/2017/10/12/q3_2017_pc_sales/ (last visited Nov 15, 2017).

- Samsung is on fire, overtakes Apple as world's #1 chip-shifter The Register (2017), https://www.theregister.co.uk/2017/02/01/samsung_apple_gartner_total_addressable_semi_market/ (last visited Nov 17, 2017).

- Cell phone sales worldwide 2007-2016, Statista, https://www.statista.com/statistics/263437/global-smartphone-sales-to-end-users-since-2007/ (last visited Nov 16, 2017).

- Laptop, PC, tablet sales 2010-2021, Statista, https://www.statista.com/statistics/272595/global-shipments-forecast-for-tablets-laptops-and-desktop-pcs/ (last visited Nov 16, 2017).

- Sejuti Banerjea, Semiconductor Industry Outlook - August 2017 NASDAQ.com (2017), http://www.nasdaq.com/article/semiconductor-industry-outlook-august-2017-cm833675 (last visited Nov 15, 2017).

- Ted Greenwald, Broadcom Bid Marks Upheaval in Chip Industry The Wall Street Journal (2017), https://www.wsj.com/articles/broadcom-proposes-to-acquire-qualcomm-for-70-per-share-1509971816 (last visited Nov 17, 2017).

- Don Clark & Tim Higgins, Qualcomm to Buy NXP Semiconductors for $39 Billion The Wall Street Journal (2016), https://www.wsj.com/articles/qualcomm-to-buy-nxp-semiconductors-1477565063 (last visited Nov 17, 2017).

- Don Clark, Analog Devices to Acquire Linear Technology for $14.8 Billion The Wall Street Journal (2016), https://www.wsj.com/articles/analog-devices-to-acquire-linear-technology-for-14-8-billion-1469563887 (last visited Nov 17, 2017).

- Don Clark, Spate of Deals Reshape Chip Industry The Wall Street Journal (2015), https://www.wsj.com/articles/western-digital-to-buy-sandisk-for-19-billion-1445427966 (last visited Nov 17, 2017).

- Ted Greenwald, Intel to Buy Mobileye for $15.3 Billion The Wall Street Journal (2017), https://www.wsj.com/articles/intel-to-buy-mobileye-for-15-3-billion-1489512027 (last visited Nov 17, 2017).

- Stu Woo & Eva Dou, SoftBank to Buy ARM Holdings for $32 Billion The Wall Street Journal (2016), https://www.wsj.com/articles/softbank-agrees-to-buy-arm-holdings-for-more-than-32-billion-1468808434 (last visited Nov 17, 2017).

- Don Clark, Dana Cimilluca & Dana Mattioli, Intel Agrees to Buy Altera for $16.7 Billion The Wall Street Journal (2015), https://www.wsj.com/articles/intel-agrees-to-buy-altera-for-16-7-billion-1433162006 (last visited Nov 18, 2017).

- Yukari Iwatani Kane & Don Clark, In Major Shift, Apple Builds Its Own Team to Design Chips The Wall Street Journal (2009), https://www.wsj.com/articles/SB124104666426570729 (last visited Nov 17, 2017).

- Tripp Mickle, Apple Sues Qualcomm Over Licensing Practices The Wall Street Journal (2017), https://www.wsj.com/articles/apple-sues-qualcomm-over-licensing-practices-1484944919 (last visited Nov 18, 2017).

- Ana Swanson, Trump Blocks China-Backed Bid to Buy U.S. Chip Maker The New York Times (2017), https://www.nytimes.com/2017/09/13/business/trump-lattice-semiconductor-china.html?_r=0 (last visited Nov 18, 2017).

Contributors to this report:Trevor Armstrong

.png.png)