Mezzanine Lending: A Strong Private Market for Financing Growth

Mezzanine financing provides alternatives to traditional capital lending and is an answer to debt managers in the credit market. As private equity transactions increase, mezzanine financing appears to be an attractive option for investors. The article will present the current trends in the mezzanine market, the outlook for mezzanine financing as well as recent mezzanine transactions in the U.S and global mezz space.

Current Trends

As direct lending is declining in the capital market, there has been a minor resurgence of mezzanine debt. The resurgence is a result of an increase in demand by dealmakers for mezzanine capital. Due to recent market uncertainty, some senior lenders are withdrawing from the market increasing the prospects for mezzanine investors.

Higher multiples are also reducing margins on attractive deals and motivating dealmakers to choose less expensive alternatives to equity. The flexibility of mezzanine debt is a factor that dealmakers are considering in structuring loans.[1] There is flexibility with structuring mezzanine coupons and covenants compared to senior debt.[2] Institutional investors are also enthusiastic about mezzanine financing due to the high yield returns and stability. There has been a surge of institutional investors purchasing higher yielding-mezzanine loans.[3]

In Europe, where lenders are moving away from traditional senior debt, issuers are slowly demanding to engage in various options for mezzanine financing. Although, the demand may not be large as its senior debt counterpart, mezzanine financing is gaining popularity.[4]

Outlook

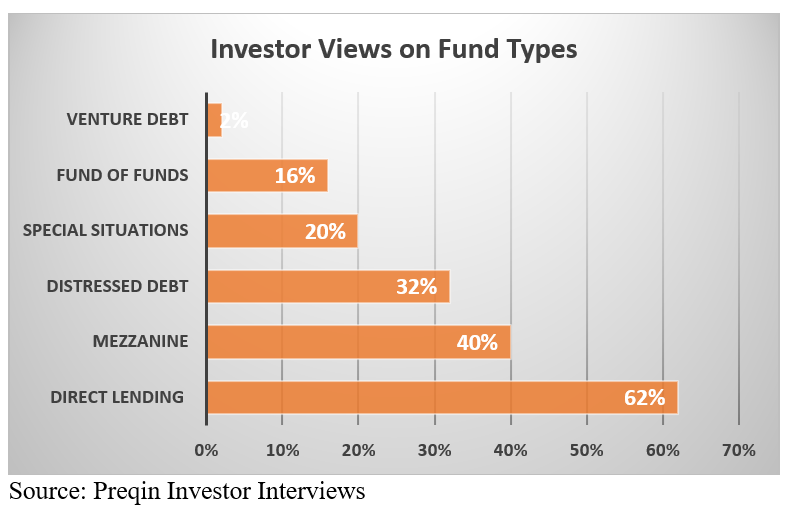

The outlook for mezzanine financing continues to be strong. Mezzanine financing opportunities are increasing both in transaction size and in frequency. In the past twelve months, mezzanine funds have become more sought after. Private debt investors have shown preferences towards mezzanine financing than most forms of debt.[5] Mezzanine debt instruments are expected to grow alongside private equity expansions. [6]

As monetary policy is exhibiting signs of reversing, there is a possibility that bank lending will decline. Leverage buyout (LBO) transactions can increase competition for direct lenders as LBO activity increases. The LBO activities can motivate bank lenders to collaborate with mezzanine lenders to secure cheaper financing capital on a “blended” basis.[7]

Mezzanine Transactions

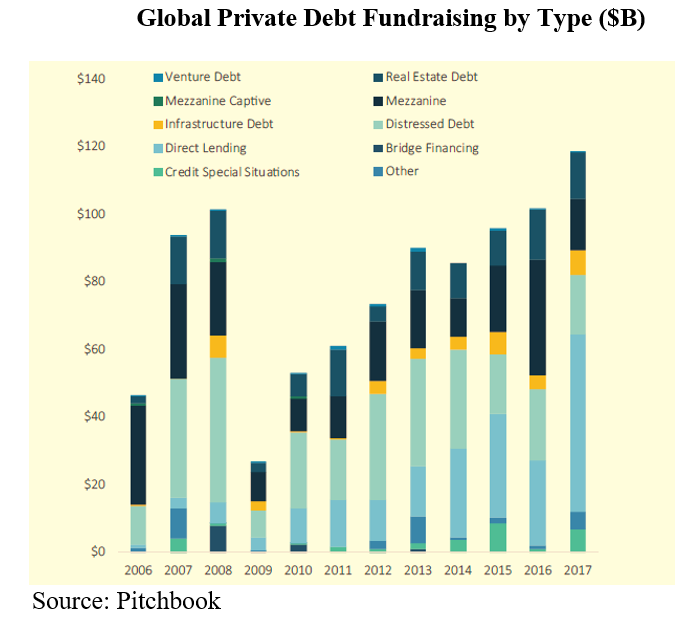

Private equity expansions have increased the growth of mezzanine debt instruments. Although in 2017, mezzanine debt transactions declined to $14.9 billion, 2016 established a record at $34.2 billion for global commitment to mezzanine fundraising. The total combined fundraising from 2016 and 2017 has been the highest mezzanine fundraising of any two-year span since 2007 and 2008.6

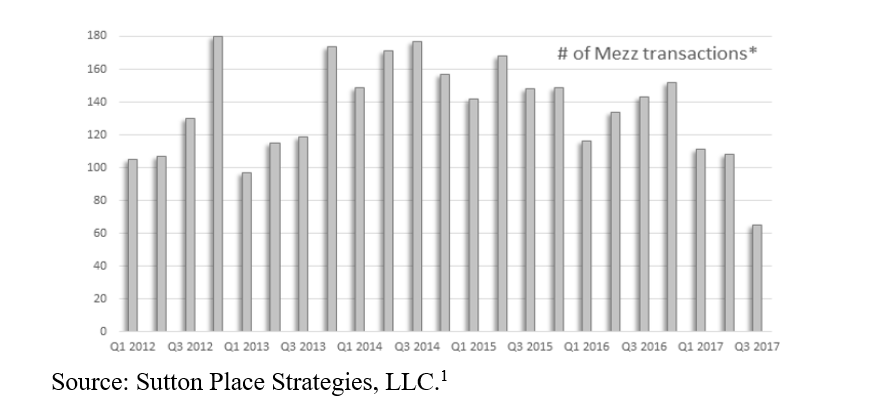

During Q2 2017, a total of 108 mezzanine transactions was completed. For the twelve month-period ending June 2017 mezzanine activity declined down by 6% from 547 to 514. Q1 and Q2 2017 showed consistency in market activity. Mezzanine transactions also declined down by 19% from 134 in Q2 2016 to 108 in Q2 2017.[8] The decline in Q2 2017 was attributed to the fact that much of the transactions in Q1 2017 were from activities in Q4 2016.[9] More than half (61%) of the transactions in Q2 2017 involved a sponsor.

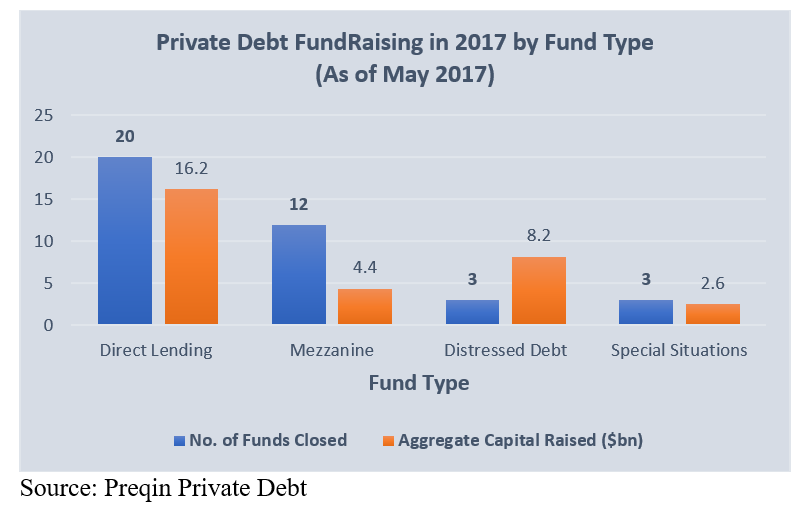

Global private debt funds increased during the first few months in 2017. The increase in global private debt was due to sustained investor interest to invest in all parts of the market.[10] More than half (65%) of global debt fundraising was from the U.S., a third (32.2%) was from Europe and 1.3% was from Asia and the remaining part of the world. During Q1 2017, five of the private debt funds were mezzanine debt while seven of the mezzanine debt were part of the private debt fundraising in Q1 2017.[11]

Conclusion

Mezzanine financing has gained popularity in recent years as investors are choosing mezzanine debt as a better-yielding alternative to senior debt due to high yield return and stability. As some senior lenders are withdrawing from the market, it is creating more opportunities for mezzanine financing. Compared to Q2 2016, mezzanine activity in Q2 2017 declined, although, Global private debt funds increased in 2017.

Sources

[1] *Select unitranche and senior debt similar to mezzanine were included in mezzanine investments.

[1] Sean Ross, Reversing Trend, Mezzanine Debt on the Rise Again, (Aug 17, 2016), https://www.axial.net/forum/reversing-trend-mezzanine-debt-rise/.

[2] CHRISTINE K. VOLKMANN, KIM OLIVER TOKARSKI & MARC GRÜNHAGEN, ENTREPRENEURSHIP IN A EUROPEAN PERSPECTIVE: CONCEPTS FOR THE CREATION AND GROWTH OF NEW VENTURES, (2010).

[3] Beth Mattson-Teig, Institutional Investors Develop Bigger Appetite for Debt Funds, NATIONAL REAL ESTATE INVESTORS, (Oct 11, 2017), www.nreionline.com/finance-investment/institutional-investors-develop-bigger-appetite-debt-funds

[4] Cushman & Wakefield, European Lending Trends, (2017).

[5] The Lead Left, Private Debt Intelligence – 8/7/2017, (Aug 7, 2017), https://www.theleadleft.com/private-debt-intelligence-872017/

[6] PitchBook, Welcome to the private debt show. Analysis of the growth in private debt fundraising, (2018).

[7] Tod Trabocco, Tracing the Rise of Direct Lending: The Importance of Rates and Loan Structure, (June, 2017), https://www.cambridgeassociates.com/research/tracing-the-rise-of-direct-lending-the-importance-of-rates-and-loan-structure/

[8] Sutton Place Strategies, LLC, Mezzanine Market Perspective, (2017), https://www.suttonplacestrategies.com/wp-content/uploads/2017/05/SPS-Mezzanine-Market-Perspective-Q3-2017.pdf

[9] Bank of Montreal, Transaction Trends, (2017), https://commercial.bmoharris.com/media/hero_image/BMOHB_TransactionTrends_Q22017.pdf

[10] Preqin, Preqin Quarterly Update: Private Debt Q1 2017, (2017), http://docs.preqin.com/quarterly/pd/Preqin-Quarterly-Private-Debt-Update-Q1-2017.pdf

[11] Pramugdha Mamgain, Global private debt funds raise $32b capital during Jan-May, (Jun 13, 2017), https://www.dealstreetasia.com/stories/74907-74907/.

Jenn Abban contributed to this report.

- Covid-19 Impact on US Private Capital Raising Activity in 2020 - May 27, 2021

- Healthcare 2021: Trends, M&A & Valuations - May 19, 2021

- 2021 Outlook on Media & Telecom M&A Transactions - May 12, 2021