How to Increase Your Business Valuation? Start With the Metrics

Experts often agree that the central issue of finance is determining a business’ value. Considering an entire field of study is devoted to valuation, analyzing the complete value of a business is no easy task. Peoples’ preferences vary dramatically, and there is no set method of valuing complex assets “correctly. In fact, no one really knows the true value of any asset, especially when it has a combination of tangible and intangible property, projected growth, and historical credibility.

Logically, the value of any business asset is the present value of its future benefit, yet the same item in the hands of different people can change the future benefit, and thus the value. For example, a guitar is worth much more to a musician, who might use it to play in shows and record albums, than it is to a baker. Now, consider hundreds of items, tangible and intangible, in the hands of hundreds of people. Herein lies the complexity of business valuation.

Volumes have been written on the subject, but an important principle to recognize is that value differs from business to business according to according to a firm’s strengths, weaknesses, and industry conditions. Besides outlining the common valuation methods and their limitations, the purpose of this article is to give insight as to how business owners might increase the valuation of their firms.

Methods

Cost ApproachThe cost method is a relatively simple valuation approach. The basic hypothesis behind the cost method is that “the price a buyer should pay for a piece of property should equal the cost to build an equivalent [property]— (Investopedia). By this definition, a business’s value is the total value of its physical assets, or “property. There are various methods of applying the cost approach.

The company can be valued using one of the following ways depending on the purpose of the valuation:Book Value: Assets are valued at “book” value (historical cost less depreciation). Book value would only be useful if valuing a company that is new or has recently been purchased. Depreciation rates are set to reflect the life of an asset, but the undepreciated value at a particular point in time is often a poor approximation of market value.Adjusted Asset: Asset value represents an estimated market value.

The challenge here is determining the value of used assets, for which there is not a strong market. This method is best used in companies where assets’ book values do not reflect market values, and there are readily available market comparisons for like assets.Liquidation: In this method physical assets are valued as if the company were to go out of business.

This method is relevant where there may be doubts about the company’s viability as a going concern. If there is a high risk of bankruptcy then the de facto value of the company may be the post liquidation market value of its assets. This can give some comfort as it can put a floor on the firm’s value. An investor may be more confident if he knows that the acquisition price is not significantly above the liquidation value.

For this reason the liquidation method is often used in conjunction with another valuation methodology. A limitation is that this method can undervalue a business that is a going concern because most businesses generate cash flows using assets that “far exceed the liquidation value of those assets (Corporate Finance Associates).Salvage/Replacement: A company is valued by how much it would cost to build an identical company.

This type of valuation would be relevant if old prices are inaccurate because new technology could allow for the same production at a lower cost. The limitation here is that a company’s complexity; with its unique combinations of assets, channels to market, employees, leaders and internal and external stakeholders, can be hard to recreate on “paper.—After pricing the assets using one of the methods above, the asset value is subtracted from the debt to determine the value of equity.

The biggest limitation of the cost method is that intangible assets, like intellectual property, effective management, and brand name are difficult to value. For these reasons, analysts may turn to other methods to determine the total market value of a company.Income ApproachThe income approach of valuation takes various forms, and each form estimates total value using a function of current earnings and projected earnings — or income.

The asset approach cannot easily measure the value of intangible or used-tangible assets, which is why the income approach is useful. An appraiser values the entire company based on expected cash flows and net income. The most common methods is the “discounted cash flow” method:Discounted Cash Flow: The discounted cash flow (DCF) method estimates value as the present value of a firm’s future cash flows after operating expenses, taxes, and interest payments.

Just as the value of a share of stock equals the present value of all future dividends, the value of a firm equals the present value of its expected cash flow. Analysts first determine the firm’s discount rate, or WACC, then estimate the earnings and cash flows from the current period. Next, they estimate future earnings and cash flows by generating an expected growth rate.

Appraisers may accurately forecast the growth direction (positive or negative), but may have difficulty estimating the magnitude of future growth. The appraiser must also estimate when the company will reach “stable growth” and the cash flows, WACC, and risk level at that point of stable growth (Damodaran).The strength of DCF is that it can incorporate the impact of a myriad of intangible assets into the valuation, including good management, streamlined processes, and a good work culture.

Since these all contributed to current earnings, they are technically factored into the model as revenue growth is estimated. The weakness of DCF is the difficulty of forecasting future results accurately. Other versions of the income approach normalize cash flow and discount rate values for simplicity. Since these approaches have more generalizations and less moving parts, they are subject to greater error than typical DCF valuations.Market ApproachMarket Comparisons: The market comparison method uses ratios from comparable companies with known stock prices.

Analysts compare a subject firm with comparable companies with known stock prices, or that have been recently sold. The approach seems easy, but small mistakes can cause significant errors in value, so often the appraiser starts by performing a DCF as a test value to assess if the “comparison” estimates are accurate. The company is then compared with multiple companies of similar size, earnings, and in similar industries by observing ratios of their characteristics.This is technical work because every company has a different operations structure, capital structure, location, and environmental factors that make it unique.

A difficulty of this method is that even though two companies may be of the same industry, size, and have the same EBITDA, they may be valued at completely different prices. For example, one may have diminishing sales in a mature economy, while the other has increasing sales in a growing economy. Placing exact values on these unique factors has proven difficult, which is why some prefer to value companies based on a driving metric, like earnings.Multiple of Earnings: Here the company value is calculated based on a multiple of earnings.

The size of multiple can be derived by comparing earnings multiples of public companies in the same industry. For example, a private company making medical devices could be valued based on a multiple in line with the medical device conglomerate Becton Dickenson. There are some inherent problems with this method. When it comes to maximizing return and minimizing risk, size matters, so a small company’s multiple will have to be scaled down when compared to a larger public company.

Great diversity of customers and products also mitigates risk. Two companies with similar revenues and income may be given markedly different multiples if their customer concentration and product diversity are dissimilar.

How to Increase Business Value

Obviously appraisers should understand each method thoroughly, but does this information benefit anyone else? The simple answer is yes. Understanding these methods will come in useful for any business owner. Valuation is performed so companies can release an IPO, sell, or price their stock options and also by investors looking for investment opportunities. Depending on the company’s industry, essential valuation metrics can differ, but here are a few things to think about to drive value as a business owner.Focus on EBITDA: EBITDA, earnings before interest, tax, depreciation and amortization, indicates the operating efficiency of a business by disregarding the effect of financing on earnings.

At a certain point, another salesman, researcher, factory worker, or software package will no longer positively impact income, and maximizing EBITDA is the strategy of finding the optimal mix of machinery, employees, research and marketing to drive profitability.This probably comes as no surprise, but the components of EBITDA are directly related to valuation.

It’s hardly a surprise that EBITDA multiples are generally used to assess valuation trends across industries. According to author Arkady Libman, the beauty of EBITDA is more than just a measure of earnings. He points out that all the components of DCF valuation, which incorporates free cash flow, growth rate, net interest rate, and discount rate, are embedded in the value/EBIT ratio (Libman).

Value = (1-t)(1-g/ROIC)

EBIT —(r-g)

You’ll notice this is identical to the formula for the NPV of future cash flows where free cash flow =(Net Operating Profit / Loss after Taxes) — Net investment:

Value = NOPLAT(1-g/ROIC)

(r-g)

The takeaway here is that focusing on EBITDA will not only increase valuation using an EBITDA multiples approach, but also for an intrinsic approach, like DCF. Thus, even when value is measured by a DCF, focusing on EBITDA (and preferably cash flow) will naturally enhance growth, return, and ultimately the company’s value.Minimize Risk: Risk is a significant component in pricing of all investments.

Even a company with a stellar-looking balance sheet and income statement looks like a risky purchase if investors do not see growth potential. Countless factors could contribute to risk including location, industry, growing competition, retiring staff, shifting trends and more. In summary, if investors have a reason to doubt the future success of a company, they will.

Consequently, the value will drop. Risk is impossible to completely eliminate, so there will always be some risk despite past performance, but there are a few ways to minimize risk and increase value. First, business owners need to prove future growth. A consistent growth trend is a good foundation, but needs to be accompanied by proof that the growth will continue.

This is why accurate forecasting should be a priority even in new businesses. Business owners should find an excellent forecasting mechanism that has proven to be accurate. A history of not only growth, but accuratelyforecasted growth inspires confidence in forecasts and reduces risk. “Another source of risk is customer concentration, so businesses should work to have a diverse, expansive customer base.

If revenue relies largely on a few big purchasers growth will be hugely impacted if just one of those goes out of business or decides to switch to another supplier.Know the Industry: A struggle with valuation is that all values are subjective. Too much focus on earnings or cash flow without regard to the industry and its position in the economic life cycle may lead to incorrect conclusions about valuation.

For example, Amazon Inc. had a negative earnings balance for years after it began, so investors who cared only about earnings would have undervalued Amazon, overlooking its other, promising characteristics. Within each industry, certain metrics are valued higher than in others. For example physical asset value has more bearing for an oil company than for a technology company, because indicators for success in each of those industries are so different.

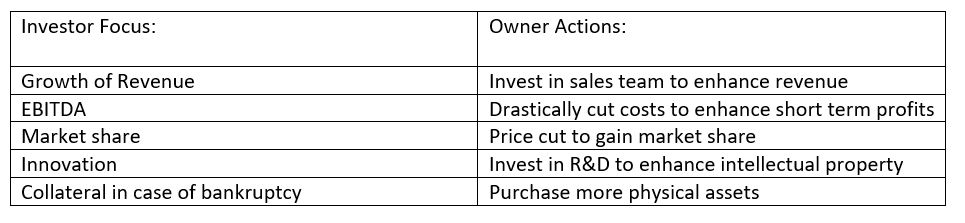

Valuations are trending upwards for 2017 across the board, so now is the time for owners to key in on the industry-specific metrics that will increase company value. Here are just a few examples of how certain industries or investors might determine value, and how an owner should respond accordingly. Keep in mind, they may not all be in the long-term, best interest of the firm.

ConclusionFirm valuation is so difficult because there are so many unknowns. The Cost method can pinpoint an exact market value on many of the physical assets but struggles to value intellectual property and other intangible assets. A DCF model values firms at a discounted value of future cash flows; however the valuation is based on forecasts and projection which are, in themselves, subjective and error prone.

The market approach gives an approximation of the value compared to other similar companies but it is hard to replicate the exact characteristics of other firms in order to determine the value.Valuation methods can vary widely even within an industry among companies of the same size. Each business is so unique, that pinpointing an exact recipe for valuation is not feasible; however, owners who pay attention to growth of revenue and EBITDA, the elimination of risk, and the key metrics that communicate value in their specific industry will have a greater likelihood of realizing their planned increases in value.

Of course business owners can live in hope that Jimi Hendrix will take an interest in their “guitar, but in the meantime they should focus on those things that can be controlled. Even though analysts have the ability to declare the price of the company, the decision makers, ultimately, have the power to for determine its value.SourcesAswath Damodaran,—Valuation approaches and metrics: a survey of the theory and evidence—(2005).Corporate Finance Associates,—CFA | Corporate Finance Associates. Business Valuation Methods | Valuation Approaches—(2017), http://www.cfaw.com/services/business-valuation-methods.html (last visited May 2, 2017).Investment Bankers talk a lot about multiples.

But what is a multiple, really?,—Wall Street Prep, https://www.wallstreetprep.com/blog/my-ebitda-multiple-is-bigger-than-yours/ (last visited May 2, 2017).Investopedia Staff, Cost Approach Investopedia (2011), http://www.investopedia.com/terms/c/cost-approach.asp (last visited May 3, 2017).

Considering a transaction?

Speak with our advisory team about your sell-side, buy-side, or capital needs — in confidence.