.png)

When an M&A transaction is underway many buyers and sellers are concerned with the terms of the deal including consideration, valuation, and any representations & warranties. While all the above are important, parties to a transaction should not forget about regulatory filings. Avoiding or forgetting about a required filing may result in extra expenses or a time delay that could impair the expected benefits of the transaction. This article takes a look at the HSR Act and how it may impact deals that could violate antitrust laws.

What is the HSR Antitrust Improvements Act?

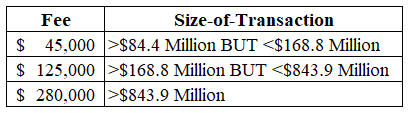

The Hart-Scott-Rodino Antitrust Improvements Act of 1976 was signed into law on September 30, 1976 by President Ford. The Act requires that companies not engage in certain mergers, acquisitions, or transfers of securities or assets until a filing has been made with the Federal Trade Commission and the Department of Justice[1]. These agencies will review the proposed transaction and approve if it is determined that antitrust laws will not be violated.When conducting a transaction that may be subject to HSR Act filing requirements the timing element should be carefully considered. Once the required filing is submitted a minimum 30 day waiting period is enacted (15 days for cash tender offers). During this time the agencies will review the submitted documents. Should the agencies require additional information they will submit a request. Once the requested documents are submitted the 30 day waiting period begins again. For buyers and sellers trying to close a deal as quickly as possible, they should strive to submit all necessary documents the first time around. An early termination of the waiting period can be requested, though the agencies are under no obligation to grant such a request.In addition to the timing element buyers subject to filing under the HSR Act should also consider the fees. The following table outlines the fees as of this writing.

[2]A final note on fees relates to penalties for non-compliance. Any person, officer, or director that fails to comply with any provision of the Act are subject to a maximum civil penalty of $41,484 (as adjusted) per day for each day in which they are in violation. These fees can quickly add up as was seen in 2014 when Berkshire Hathaway was required to pay $896,000 in fines.While fees can certainly be hefty the FTC and DOJ can decide to waive fees for the first violation. This is done when it can be demonstrated that the failure to file is due to simple negligence and the parties submit a corrective filing immediately. The company may not have benefited from the failure to file and it must be their first violation of the Act.

The Three Tests of the HSR Act

While we have thus far outlined the requirements and fees associated with the HSR Act, we have not identified when the filings must take place. A premerger notification is required under the HSR Act, assuming no exemptions have been met, if the transaction meets the following three tests[3].1. Commerce TestThe easiest of the three tests and one that most companies will pass. If either party to the transaction is engaged in commerce or any activity affecting commerce, the test is satisfied.2. Size of the Transaction TestThe size of the transaction test requires the parties to determine the value of the proposed transaction and file accordingly. The thresholds are adjusted annually so it may be necessary to check with an adviser for your specific transaction. As of 2018 the thresholds were as follows:

- Transactions less than $84.4 million are not required to file

- Transactions valued at more than $84.4 million but less than $337.6 million must be reported if the size of the parties test is met

- Transactions value at more than $337.6 million must be reported regardless of the size of the parties

Determining the size of the transaction is a complex procedure and it would be wise to seek professional assistance when starting down this path.3. Size of the Parties TestThe size of the parties test is met if one party has at least $16.9 million in assets or annual net sales and the other party has at least $168.8 million in assets or annual net sales.While it is important to comply with the HSR Act requirements it is wise to determine if a specific transaction is entitled to an exemption. Remember, the purpose of the Act is to prevent the violation of any antitrust laws. Transactions that are deemed unlikely to break such laws may be exempt from filing.

How to Manage Your Transaction in a Compliant Manner

Companies entertaining the idea of a transaction should carefully consider any filing requirements that they may have to comply with. Antitrust considerations should be evaluated during the due diligence phase by lawyers conducting an antitrust analysis. This analysis will aid in determining the risks associated with delay and even non-completion of the deal. This is of particular importance to buyers who may be required to pay a breakup fee should the deal not be able to close due to antitrust issues.The following is a short list of antitrust considerations when planning a transaction. While by no means an exhaustive list, it should suffice to get potential buyers thinking along the correct lines when considering a deal.Notification RequirementsThe Hart-Scott-Rodino Act has been discussed above. Parties to a transaction should begin analyzing if they will be required to file before the transaction takes off. Depending on the location of the involved entities foreign filing requirements should also be reviewed.Gun JumpingGun jumping may occur if a party takes possession of securities or assets without adhering to the waiting period under the Act. To avoid this scenario the companies involved in the transaction should continue to operate as independent entities until the waiting period has ended and the FTC and DOJ have concluded their review.A second form of gun jumping is possible. Under this scenario the parties to the transaction appear to be working together prior to the close of the transaction. This may pose an issue under Section 1 of the Sherman Act[4]. While due diligence is an understandable necessity, the parties should tread carefully. If competitively sensitive information must be exchanged, then consider using clean teams. It is also important not to begin any integration efforts, outside of planning, until after the deal closes. When in doubt speaking to an antitrust lawyer is the best course of action.For those of you that have gone through the process of filing and complying with the HSR Act, do you have any advice to share regarding your experience?[1]15 U.S. Code � 18a - Premerger notification and waiting period, LII / Legal Information Institute, https://www.law.cornell.edu/uscode/text/15/18a (last visited Apr 9, 2018).[2]Filing Fee Information, Federal Trade Commission (2018), https://www.ftc.gov/enforcement/premerger-notification-program/filing-fee-information (last visited Apr 9, 2018).[3]Steps for Determining Whether an HSR Filing is Required, Federal Trade Commission (2013), https://www.ftc.gov/enforcement/premerger-notification-program/hsr-resources/steps-determining-whether-hsr-filing (last visited Apr 9, 2018).[4]15 U.S. Code � 1 - Trusts, etc., in restraint of trade illegal; penalty, LII / Legal Information Institute, https://www.law.cornell.edu/uscode/text/15/1 (last visited Apr 9, 2018).

.png.png)