With a period of sustained low-interest rates, investors and corporates have started to look towards M&A as a way to increase investment returns. This has amplified demand and facilitated an increase in deal valuations. Recent data suggests there are no signs of this growth slowing. Valuation multiples, in North America, have been consistently ticking up since 2009.

Increasing from the low of 6.4x in 2009, a residual effect of the financial crisis, to a solid 10.6x on deals completed through 3Q 2017 1.The importance of valuation multiplesComparing company based valuation multiples is generally what analysts and investors use for a quick snapshot of a company or an industry. They are great at looking at trends and giving you a rough understanding of what the market has decided a company is worth.

In periods of inflating multiples, investor confidence increases thus driving further increases in valuation multiples. It works the opposite when times head south. However,—like with most valuations methods, multiples can be misused. A common misuse is the calculation of an industry-average price-to-earnings (P/E) ratio, multiplied it by company earnings to establish a "fair" valuation.

The use of these industry averages overlooks the fact that companies in the same industry can have radically dissimilar anticipated growth rates, returns on invested capital, and capital structures. Make sure you are comparing apples to apples.For these reasons, managers enthusiastic about maximizing shareholder value, tend to favour the classic discounted-cash-flow (DCF) analyses as the most accurate means of valuations.

Properly performed, which we will discuss in a blog later this month, such analysis can help any company stress-test its cash flow forecasts. As a firm seeks to explain why its multiples differ (whether higher or lower) than those of its competition, it can generate insights into the key aspects driving value into an industry.Positive headwinds are here to stayThe increase in valuation multiples cannot be attributed to a single factor.

In general terms, the driving factors will include a combination of sustained low-interest rates, which translates to cheap debt and a low market risk premium, platform roll-ups, and large cash reserves on corporate balance sheets. These factors have not only contributed to record high index values in the stock market, they have flown into the private markets as well; in particular with increased M&A activity.Accounting practices tightenAlthough red tape can lead to inefficiencies, following the financial crisis of 2008 corporates have had to tidy up their accounts.

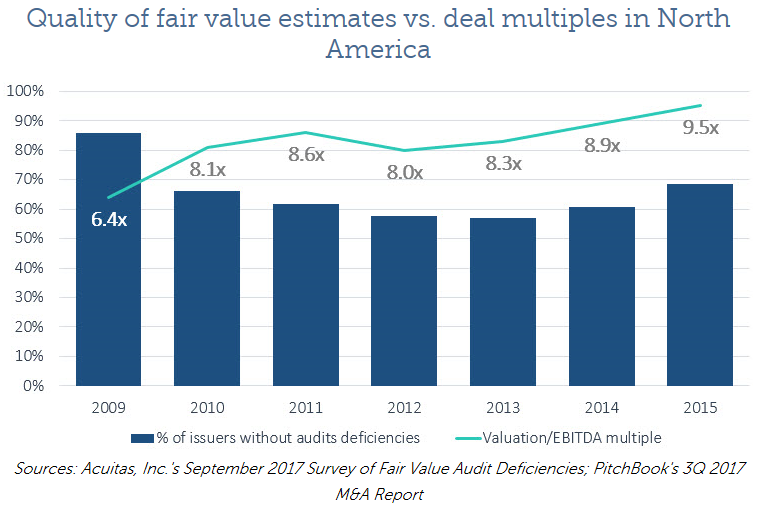

We have discussed grey areas, like goodwill, in previous blogs but several other lines in financial reports can and have been manipulated historically. 'Big brother' looking closer at what companies are doing in their financials has had positive outcomes. Firms are required to provide more information on fair value items, and these items are now required to be broken down to provide improved insight.

This has consequently improved investor confidence that the fair value estimates behind increased deal pricing are accurate. This has aided multiples, as the valuation discount associated to risk has decreased.

Audit deficiencies are downAudit deficiencies, “a deficiency, or a combination of deficiencies, in internal control over financial reporting that is less severe than a material weakness, yet important enough to merit attention by those responsible for oversight of the company's financial reporting, are a key indicator to investors”2, are down. These deficiencies have dropped in recent years, thanks to increased focus on fair value reporting of the nonfinancial assets that often make up a key portion of M&A deals especially in fast-growing companies where "goodwill" and intellectual property comprise the bulk of the combined value.In short, management bias is the large cause of these historic inefficiencies, and different managers have different boundaries they have been willing to push, leading to more uncertainty. We have seen a shift in the source of most audit deficiencies from hard-to-value “black box” financial assets, to categories related to business combinations and international subsidiaries.

This is important because of the quick pace of M&A activity in recent years has meant investors need to analyze this in more detail.What does this mean if you want to sell your business?We covered off how to always be prepared to sell your business on a previous blog. You never know when someone will approach you to acquire your business, it’s generally unexpected.

In short, your company should always be running in tip-top condition, and the accuracy and clarity of your financials will boost your valuation. Investors are becoming accustomed to more clarity on items like goodwill and depreciation, so you should do the same. Manipulating the numbers to increase profits in one year, may have issues with your selling price in future, it’s a balancing act.Is now the time to sell?The world seems to be both fascinated and fixated with cryptocurrencies, with little discussion about increasing M&A multiples. It is a good time to sell a business or for that matter is a great time to be a target.

Valuation multiples are high, and management teams looking to sell should be open and truthful in their accounts, in particular with their fair value assumptions. Cash is king, but confidence, or lack thereof could be the straw the breaks the camel's back.1 Improved valuations unlock higher deal multiples, PitchBook News, https://pitchbook.com/news/articles/improved-valuations-unlock-higher-deal-multiples (last visited Jan 9, 2018).2 Auditing Standard No.

5’ //, Auditing Standard No. 5, https://pcaobus.org/Standards/Auditing/Pages/Auditing_Standard_5_Appendix_A.aspx (last visited Jan 9, 2018).

Considering a transaction?

Speak with our advisory team about your sell-side, buy-side, or capital needs — in confidence.