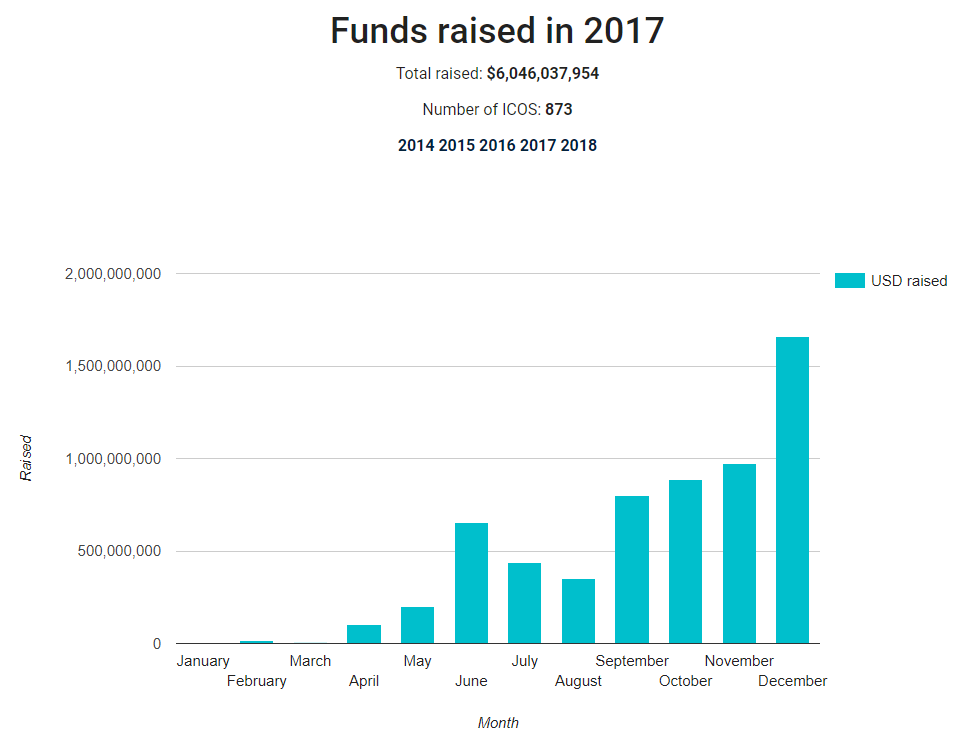

If you were anywhere in or around the crypto-sphere in 2017 you might have been wondering what in the world was going on. Securities, re-branded as tokens, were being sold to anyone that knew how to spend cryptocurrency in unregistered offerings called Initial Coin Offerings (ICOs). Millions of dollars were being raised on hopes, dreams, and the infamous whitepaper.

[1]Source: ICOdata.ioIf you stopped and asked where were the regulators you may have heard something along the lines of "where we're going, we won't need regulators". That was 2017. Regulatory agencies, such as the SEC, were not asleep at the wheel and they have been busy this year demonstrating just that. Do they move slowly? Sure, but they do move.One of the most recent movements we have seen pertains to cryptocurrency exchanges such as Coinbase, Circle, and Bittrex.

While these exchanges may require users to supply identifiable information when creating an account, they are not registered as national securities exchanges or broker-dealers. Why does this matter? The SEC has made it clear that a platform that functions as an exchange and desires to list tokens that have been classified as securities will need to either register as a national securities exchange or operate under an exemption.

Given that SEC Chairman Jay Clayton has made his stance on the security vs. utility token debate rather clear (hint: he says security) it would be wise for exchanges to start figuring out how to comply with regulations. One option many exchanges seem to be interested in pursuing is the alternative trading system.

Alternative Trading Systems

At its core an ATS is a platform for matching buy and sell orders of its users. An ATS does not set rules for its users, outside of rules of conduct, and usually registers as a broker-dealer. An alternative trading system serves a very important role in providing investors alternative means to access liquidity. Equity positions in early stage startups have little or no liquidity, preventing investors from realizing a return on their investment for several years.

Bringing together security tokens with an ATS may help solve this issue. Once registered ATS platforms are available investors will be able to buy and sell security tokens that have been created by issuers who used an existing exemption. Investors may still be subject to holding periods per Rule 144, but a one year mandatory holding period is better than a 3-5 year period due to lack of liquidity.

For cryptocurrency exchanges that would like to list tokens that are classified as securities, registering as an ATS will help keep them on the path of compliance. This includes registering with the SEC as a broker-dealer and becoming a member of a self-regulatory organization (SRO), such as FINRA. They will also be required to file applicable paperwork, such as Form ATS.

It is refreshing to see that some exchanges are already beginning to do their homework on how to comply with the SEC's rules. On April 6th an article in The Wall Street Journal discussed Coinbase and their efforts to become a licensed brokerage and electronic trading venue.

Regulation ATS

In 1998 the SEC introduced Regulation ATS. As with many of the regulations put in place by the SEC the reason behind implementing Reg ATS was investor protection. It was also needed to address the new electronic trading systems that were becoming more popular at the time. Under Reg ATS an ATS must register as a broker-dealer and must file an initial operating report (Form ATS) with the SEC 20 days before beginning operations.

Form ATS requires a litany of information including:

- Securities the ATS expects to trade;

- The manner in which the ATS operates;

- How subscribers will access the trading system;

- The class(es) of subscribers and any differences in services offered to each class;

- Procedures for order entry and execution

So, what does all of this imply for the cryptocurrency world? It means that exchanges, issuers, and investors will all be impacted in some way.1. Exchanges: Those that are running exchanges will need to start researching how to comply with regulators. That may include becoming a registered ATS or finding some other exemption. This will have costs and ongoing reporting requirements.

Changes will need to be made. The SEC and SROs are in the business of protecting investors and will take the necessary measures to do so.2. Issuers: In 2017 a company could launch an ICO, raise a boat load of money, and be on an exchange the next day. That will most likely not be the case going forward. Since exchanges will be making an effort to comply with regulators and the rules of operating an ATS, they may become more selective in which tokens they list.

It is reasonable to predict that the exchanges will only want to list tokens that were issued under a securities exemption, such as Regulation D. A security token that was not issued correctly and that did not implement proper KYC/AML procedures will be a liability for an exchange. To this end, we should begin to see more issuers using the allowed exemptions.3.

Investors: New regulations may come with extra costs for the exchanges and issuers. However, the investors stand to greatly benefit. One of the benefits of exchanges becoming registered is that they will be required to meet minimum standards regarding operating procedures and checks and balances. While it wouldn't be reasonable to say that all fraud will be extinguished via regulation, it is hoped that fraudulent and dishonest practices in the industry would be reduced.As we move away from the Wild West of 2017 crypto and into more regulated waters some people will be happy, and others will try to fight the regulations as long as possible.

It is this writer's opinion that leaders in the blockchain and crypto community should take this opportunity to work with regulators. Some existing laws may work while others need to be revised to fit the new technology. It may be that we need some new laws entirely. Regardless, working with the agencies responsible for investor protection will allow the industry to mature and become more widely adopted sooner rather than later.Sources[1]ICOdata - ICO 2017 Statistics. (n.d.).

Retrieved April 21, 2018, from https://www.icodata.io/stats/2017

Considering a transaction?

Speak with our advisory team about your sell-side, buy-side, or capital needs — in confidence.