.png)

As the buyer in a transaction you will have a long list of items to request from the seller during due diligence. One area of particular importance has to deal with the seller's assets and any liens against those assets. Even when a transaction is structured as an asset sale, any liens on the seller's assets will become your problem.

What is a Lien?

A lien is a legal right or interest that a creditor has in another individual or entity's property. For buyers, this means that if you purchase assets that have a lien against them, someone else has an interest in your newly acquired property. This other party may be a creditor and that could spell trouble if the lien is still intact once the deal is closed. It is possible to include language in the purchase agreement that will protect you. However, I recommend conducting thorough due diligence on your target as your first line of defense. Thankfully, searching public records can clue you in as to any liens.

Types of Liens

In this section we will review three types of liens:1) UCC Liens2) Tax Liens3) Judgment Liens

UCC Liens

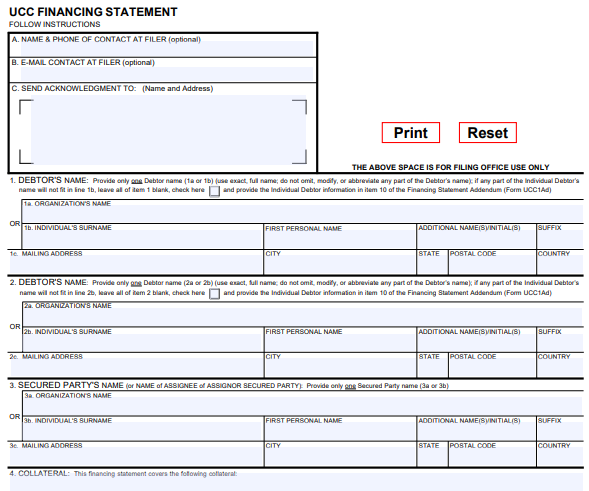

The Uniform Commercial Code (UCC) is a collection of established rules governing how commercial transactions work in the United States. It is from the UCC that we get the term UCC lien. As I mentioned above, a lien is a security interest that a creditor has in another's property. UCC liens are not bad in and of themselves. On the contrary, they are normal in the course of business. A lien may arise when securing bank financing, receiving trade credit for equipment, or when purchasing real estate.A UCC lien may be placed on a business when it enters into a financing agreement that is secured by collateral. The lien is put in place to serve as a notice to other potential lenders that the business owes money to a lender and that the business's assets are pledged to the lender until the debt is repaid.The filing of a UCC typically begins when a business pledges assets to a lender by signing a security agreement. Once the security agreement is signed, the lender will file a UCC lien against the pledged assets. UCC liens are a first come, first served position. What this means is the first creditor to file a UCC lien against a specific asset will be first in line to collect on the asset if a default occurs.UCC liens are necessary to protect lenders from borrowers who may try to secure several loans collateralized by the same asset. For example, a manufacturer who tries to take out three loans using the same piece of equipment as collateral. Prior to UCC liens this would've been possible since none of the lenders knew about the others. Now, it is possible to search public records to see what assets are available as collateral and which already have liens against them.UCC liens can be further broken down into two flavors: specific collateral and blanket.A specific collateral lien is when a lender has an interest in one or more specified assets, but not all of the assets owned by the business. This style of lien is common when a loan is for a specific purpose, such as equipment or inventory financing.Blanket liens occur when the lender has a security interest in every asset owned by the business. If a blanket lien is filed, it may be difficult for a borrower to receive any additional financing until the debt is repaid. This style of loan is more common with traditional banks loans and SBA loans when the lenders wish to fully secure their loan. Lenders generally like blanket liens, as it gives them an interest in all the assets owned by a business. For a borrower, agreeing to a blanket lien may allow the lender to be more flexible with underwriting and provide funding faster.A lienholder will perfect their interest by filing a UCC-1, also called a financing statement. This form includes information such as the legal name of the debtor and creditor and a description of the collateral. The following is a UCC-1 form:

Tax Liens

Unlike UCC liens, which shouldn't be an immediate cause for alarm, a tax lien should be a red flag for any potential buyer. A tax lien is filed by the IRS when a business doesn't pay its taxes on time or in full. The lien is generally on all the business's property, which includes AR and any assets acquired in the future while the lien is in effect. In addition to the IRS, state and local taxing authorities are also able to place a lien for unpaid state and local taxes.Tax liens are filed at the company's place of business, where the executive offices are located. This varies from UCC liens which are filed in the state of incorporation.

Judgement Liens

A judgement lien is put in place after a person or business loses a court case and has a judgement entered against them. Judgement liens can be placed on real estate, personal property, vehicles, and property acquired after the lien is put in place. If the lien is attached to real estate, the real estate must be in the county where the lien is recorded or where the judgement was entered.

Searching for UCC Liens

As a potential buyer, you have a few options when conducing a UCC lien search:1) Do it yourself2) Use a third-party serviceI would advise most buyers to use a third-party service, unless they have extensive prior experience conducting UCC searches.If you opt for the DIY method, you can search the state UCC records for liens online. Alternatively, you can also file an Information Request using Form UCC-11.When conducting your search, be sure you are using the seller's exact legal name. If you are unsure of the correct legal name, consult the Secretary of State's business entity database in the state where the business is incorporated.If you opt to use a third-party service, it will be a welcome to learn that they are affordable and can generally conduct tax and judgement lien searches at the same time. As a buyer, you will have your hands full with a multitude of other tasks. Allowing professionals to conduct the lien search for you is generally a better use of your time and efforts.What happens if the UCC search uncovers a lien filing? First, be glad you conducted the search! Next, determine if the filing has been terminated or if it is still active. If the filing has been terminated, this indicates that the borrower has paid off the debt. However, if the statement is active then you need to work with the seller. It will be critical to ensure the lien is closed or released prior to closing the transaction. If the lien isn't closed or released, the creditor will have a security interest in your business assets post-close. This is not an ideal situation.

How a UCC Filing Impacts Your Business

Generally, a UCC lien won't have a negative impact on your business, assuming you don't need to borrow additional capital and that you don't default. However, there are a few risks that should be considered when it comes to UCC lien filings.

Difficulty Borrowing

A UCC lien may prevent your business from receiving additional financing prior to repaying the debt. The lien may reduce the chances that your business can qualify for traditional and alternative loans.As mentioned above, UCC liens are a first come, first served position. It may prove difficult, or impossible, to convince a lender with an existing lien on your assets to carve out some of their security interest for another lender.

Your Credit Report

UCC liens from the past five years will show on your business's credit report. While the presence of lien will not impact your score, it may figure into lending decisions after a lender reviews the report. While the lien itself won't impact your score, the actual loan, along with the payment history, will.

Losing Pledged Assets

When assets are pledged as collateral for a loan, the business runs the risk of losing those assets if they default. If a UCC lien is filed, then the assets used as collateral should be considered at risk until the loan is repaid.For buyers of a business, liens may pose a significant risk. A diligent buyer will conduct proper due diligence by including a UCC, tax, and judgement lien search prior to the close of every transaction.

.png.png)