.png)

We are often asked, "what do you charge for raising capital?" The short answer: the cost of capital is extremely deal dependent. The investment banking fees charged for raising debt and equity differ widely from�fees charged for sell-side M&A. Additionally, on a dollar-for-dollar basis, the middle-market pays more for financing than larger counterparts. That cost, is very dependent on a number of factors, including timing, deal preparation, type of capital, type of investors and deal size. Here we outline a few of the various dials which may have an affect on the cost of�a capital raise.

Debt or Equity

The cost of� capital�pivots�on whether�the company is�seeking debt, equity, mezzanine or whatever the latest facility the peddlers are pitching. In today's Fed-fueled world, where debt is cheap, it is difficult for investment bankers to charge bulky fees for debt, even if such fees are grossed-in to the overall loan. In addition, debt can often be easier to source, particularly if an existing balance sheet is light already or the earnings can easily service the "ask." Engagement fees�requirements for debt�are also less likely�as it remains less of a sunk-cost risk for the ibanker.On the equity side, there frequently remain costs for both engagement and contingency. How such costs are delineated are dependent on whether the capital is sourced from institutions and what the size of the deal is.

Institutions vs. Individuals

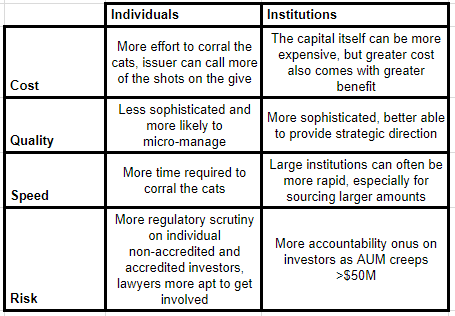

We�have said it before: institutions are faster and more sophisticated when it comes to raising capital. They are also less risky, from a regulatory perspective. The following graphic should be somewhat helpful in showcasing the cost, quality, speed and risk differentials between individual accredited investors and institutions.

Most investment bankers are likely to charge more for preparation and outreach to individual accredited investors than they will to institutions.� Individual investors typically fail in all the following ways as well:

- Less sophisticated. While they may be doctors, dentists, entrepreneurs and lawyers, they are less likely to be a quick study on the specifics of an investment, typically requiring more time to assess. On the institutional side, an entire team helps make the assessment on whether or not an opportunity is a fit for a fund.

- Unprofessional. This is not meant to be a jab. While such investors may be professional in their own sphere of influence, they are likely not "professional investors." That is, they do not spend their days actively seeking to place dollars in an effort to elicit a return. Consequently, they require more chasing and are generally seen as more lackadaisical.

- More documentation. Typically individual investors require more documentation in a deal than a simple pitchdeck.�Not only is the outreach to individuals itself a bear, but regulation often requires more preparation for adequately disclosing the risks to individual investors (e.g. Regulation D and its associated rules).

These are only some of the reasons, accredited investor equity crowdfunding has failed. The post-and-pray platforms have done a good job selling hype, but in the end they have failed to live up to the promise of cheaper capital. Such deals require more outreach, more effort, more documentation and greater marketing--all of which have a measurable cost. What good is capital that requires less of an equity give (in this case, accredited investor funding through Reg D) if�said funding requires greater effort and higher risk to source?�When weighing all the costs involved, the�decrease in the equity give is likely not worth the added cost of bringing incremental equity slices of say $25K to $50K into the deal.

Deal Size

For both�engagement and contingency fees, the dollar-for-dollar capital cost of raising equity significantly decreases the greater the amount to be raised. You could liken it to a bulk discount. Most investment banks have their minimums for raising capital. But, that does not mean an issuer should bloat the sources and uses to reach the internal size threshold of his or her investment banker. Here is an example of an oft-repeated conversation that illustrates this very point:Potential client: "I am looking to raise $1M to fund _________."�Investment Banker: "I am sorry, but our minimums for raising equity are $10M."�At this point the potential client has been known to say at least one of the following:

- "Well, we could use $10M. What if I hired you to raise $10M instead of $1M?"�

- "I have this other idea..." [don't get me started on this one]

- "If you can do $10M, $1M should be easy."�

There are different flaws in each of these rebuttals, but the�greatest truths of consideration on deal size are these:

- Smaller deals take as much (and more often more) time than larger deals.

- Smaller deals are more difficult to complete. They are likely not as sustainable and more early-stage. The greater risk means less interest from institutions. Yes, there are venture capitalists that could have interest, but the bulk share of the private markets is not in venture capital.

- Smaller deals are more risky (see previous point above).

It becomes a true case of catch 22. Regulation D private placements need more hand-holding, more outreach and more effort (something which most of the 506(c)-geared platforms do not provide), but such effort is not expended unless you pay a licensed third-party intermediary to assist in the "finding" of investors--a proposition which requires even more capital. Bear in mind, this all comes with the empty promise of a "best efforts" offering, which means there is a high probability of failure. This is why raising capital is so hard.

Transaction Timing

It is a simple fact that a desire to increase speed also increases costs and--unless properly policed--it can have a detrimental impact on�quality. I always cringe when issuers say something like, "we need $XX,XXX,XXX.XX and we need it in the next 60 days." We are certainly accustomed to the hustle, but when capital timing hits emergency status, the costs to�engage an investment banker increase.�Understanding the cost, quality speed trade-off�is important when it comes to nailing your cost to source capital.

Level of Preparation

As previously stated, the type of offering will impact the amount of requisite paperwork required. Individual, accredited investor offerings require greater disclosure. In such cases, issuers may be required to have a Private Placement Memorandum (PPM) and other requisite offering documents drafted by a securities attorney. Unfortunately, the vast majority of would-be issuers are nowhere near prepared to raise capital from individual or accredited investors. Lack of preparation on an issuer's part, requires more work on the investment banker's (and sometimes the attorney's) part--which includes a higher cost.�Issuers' pitchbook preparation is all too often lacking. When that is the case, it is likely well-advised to hire a professional to draft something worthy of investors' attention.While we have failed to make mention of actual costs up to this point, here are a couple of pointers to help lower the cost of raising capital:

- Come prepared. Do not bring the proverbial knife to the VC gun fight.

- Know your investor audience. Know where the money is. While investment bankers have great databases, if you already come having done your homework, marketing the deal is that much easier.

- Provide a time buffer. Do not let the capital raise become an emergency.

- Know what you want. Understand the differences between debt and equity and the relative differences in costs for sourcing them.

In the best scenario, when an issuer is prepared enough, they do not even need an investment banker. In fact,�that is exactly the intent of our�fintech software platform---dis-intermediation of investment bankers. Until we use Artificial Intelligence (AI) and other advanced technologies to�completely eliminate�the need for knowledgeable advisory, investment bankers will still work to add value in capital transactions. While the bankers would love to add value in each scenario, some deals are on the hopeless end of the spectrum. Even some of the most quality deals still require a great deal of deal preparation. Few dealmakers will prepare and promote a deal without charging some type of consulting fees. Where are you on the preparation spectrum?If you are looking to raise capital, we would love to learn more about your project details, learn if there is a fit and--if so--provide a meaningful proposal and statement of work. We look forward to working with you.

.png.png)