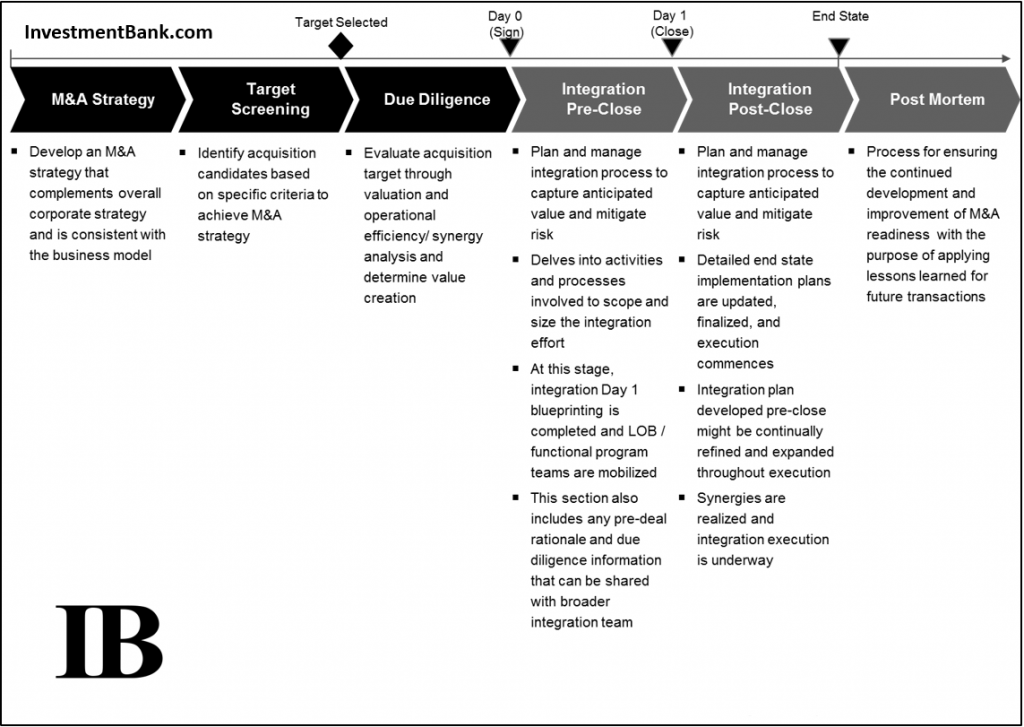

Buy-Side M&A: Pitfalls & Opportunities of a Successful Acquisition Strategy

The ethereal concept of �synergy� and �value add� are certainly less prevalent in mergers and acquisitions than many deal peddlers would have us believe. Creating the 1+1=3 scenario in M&A requires smarts, discipline and a large focus on planning�areas where many investment bankers and deal integration teams fall short. More than just a simple exercise of enumerating �cost savings� and �revenue generating� activities between two initially siloed entities, successful M&A requires focus on detailed minutiae including a focus on asset value maximization (human, fixed and technological), customer value enhancements and, of course, redundancy elimination.

Here we will discuss just a few of the critical success factors in M&A, how transactions can be seriously botched and how to avoid the botching and realize the true goal of strategic transactions: value maximization.

Executive Leadership

Certain activities in M&A can never truly be outsourced or delegated. Too often C-level executives fail in this respect. Entrenched and committed executive involvement throughout the acquisition process does more than ensure true ownership of the tasks and projects, it sends a non-verbal cue to those driving toward close and successful integration. A strong endorsement and sponsorship from the C-suite creates an atmosphere that lends itself to success.

Heavy lifting by lower-level deal and integration teams is best accomplished when leadership signals strong buy-in on the buy-side.Furthermore, executive alignment of goals, processes and the thesis for performing strategic M&A tilts toward a pattern of success. Alignment is required between executives on the buyer side, the seller side and jointly between buyer and seller.

Such alignment requires regular communication of expectations. Nothing should be left to assumption. Additionally, a chain of command and project accountability (which is helpfully accomplished through our project management software solution) can help prevent disgruntled employees, value erosion and employee turnover. Ultimately, employees and managers of a successful buy-side process will send the message that deal integration is the most important item on everyone�s agenda.

Deal Planning

With executive buy-in deal integration teams will face hurdles toward realizing expected synergies between two organizations. Recognizing such will require a detailed analysis and strategic rationale for the �how�, �what� and �why� long before the �when�. That is, business issues, customer analysis and soft deal considerations (like customer and employee culture fit/clashes) should all be on the discussed and planned long before their actual attempted integration takes place.

It�s the old �fail to plan, plan to fail� conundrum. From branding issues to customer on-boarding, the processes and procedures for integrating require detailed analysis and proper planning, then execution. In fact, in some instances it can be safer to silo the organization and wait to integrate until sometime after a deal closes. This can help to relieve the issues of executed on a half-baked integration scheme.

Of course, it still requires setting expectations among employees who may feel their positions are threatened as a result of the deal�a delicate balance that should be carefully weighed.With the timing of integration in mind, there is often a heavy focus on �day one� metrics. Investment bankers are notorious for a tunnel-vision focus on the closure of a deal.

His/her compensation is the main motivating factor toward ensuring a successful outcome and thus the focus on pushing toward closure. Integration teams can help provide the balance of focus, driving internal stakeholders to drive on other items like preserving existing cash flows, creating value enhancements and realizing expected synergies. Stabilizing the separate entities and focusing long past �day one� and the transaction close will aid the newly-merged companies in avoiding some of the pitfalls associated with post-merger integration.Process management of due diligence and post closure integration includes detailed task creation, assignments and accountability monitoring, as well as the post-close 100-day plan.

It brings numerous, differing stakeholders in finance, marketing and operations from two separate entities, including all the complexities associated with integrating systems and processes. Detailed steps that outline the expected deal value drivers�including cost savings and revenue drivers�are typically papered, assigned and monitored using deal integration and technology tools.

Additionally, several key stakeholders are assigned the task of ensuring value preservation among the two separate entities. This could include ensuring the avoidance of losing key employees, customers and overall goodwill in either of the two entities. It can take a lot of cost and revenue synergies to make up for losses if existing revenues are among the two entities are not properly preserved.

If executed properly and managed from competent leadership, value-preservation plans that start day one can have a huge impact on the long term success of a deal.

Tech Working for Deals, Not Deals for Tech

Deal success in today�s world is both managed by and harangued by technology. Critical to the integration success of any deal is the successful integration of both company�s IT systems. Additionally, information technology including advanced data room and project process tools can be used to manage the integration itself. In today�s world, successful accomplishment of anticipated deal objectives requires both integration of IT in M&A and the use of it.

The tech can be an enabler, but if not done properly, it can be a major hindrance to the original deal objectives.

Failure to Operate

There is a death zone in buy-side M&A that can negatively impact and/or reverse any potential synergies had in a deal. Failure to properly operate the business as a going concern throughout the due diligence, close and post-close period is likely to result in some type of value destruction. This can occur due to executive neglect, management neglect or employee neglect.

Even more rare is the potential for leaked information about a deal that could scare customers and suppliers. Executives and managers can get distracted from the day-to-day while employees may have legitimate fear of potential job loss.Keeping the potentiality of a deal under wraps until after close and integration plans are well on their way can be difficult, especially when specific people within the company are likely to be working on tasks relative to the deal.

Control what you can, but exercise caution. The worst thing that could happen is damaging the existing company by refocusing key operational personnel into M&A. Hiring an investment bank or internal deal makers can help save heartburn in the interim.

Soft�Deal Points

People and culture issues can plague even the best deals. Employees may feel threatened, lack of clear communication from executives and the overall �unknowns� that accompany employees in a transaction can prove fatal if not properly managed. Early identification and resolution of cultural issues among employees in both pre and post-close phases can ensure the businesses at least maintain the status quo�ensuring revenues and cash flows remain intact.

Business stabilization and change management issues are critical at every juncture.Avoiding the soft issues that come with deal integration requires communication. Regular updates on the status of the deal, how the deal will impact employees during and following the close and what they can expect in terms of workload can all play a critical role in deal maintenance.

In short, success here is a matter of communication, communication, communication.Closing the gap between potential realized synergies is often an overlooked merger integration planning exercise that ideally begins long before a target acquisition is even in the cross hairs. Unlike sell-side mergers and acquisitions, buy-side deals include more moving parts in the integration process.

If one waits until due diligence, the window has passed and the potentiality of larger mistakes increases substantially. Volumes could be written on the pitfalls and processes inherent to a buy-side M&A deal, but covering the �big rocks� is an absolute necessity.

Considering a transaction?

Speak with our advisory team about your sell-side, buy-side, or capital needs — in confidence.