.png)

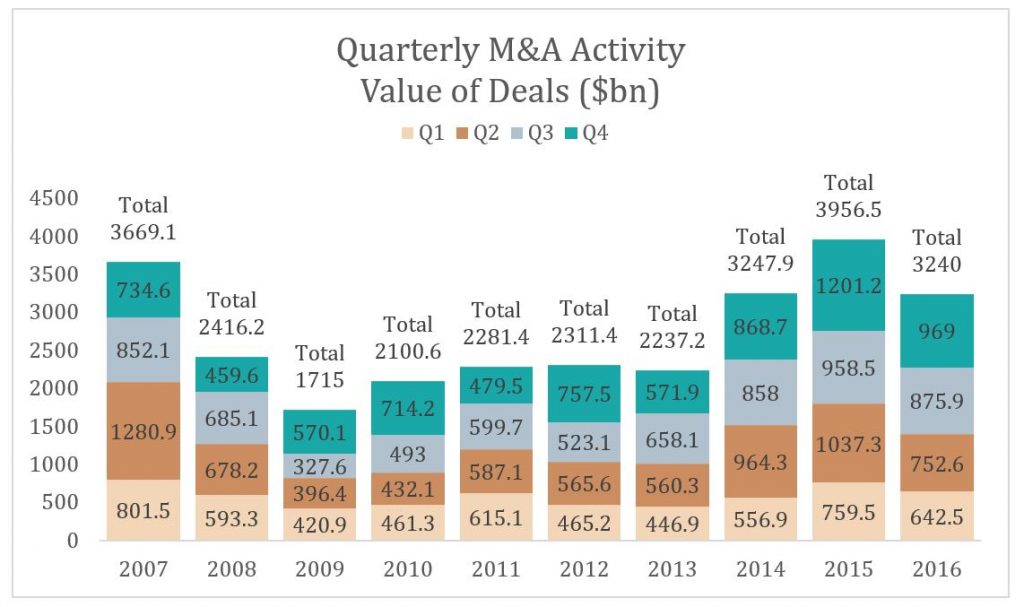

M&A continues to thrive--Global mergers and acquisitions reached $3.2 trillion in 2016, marking the third best year with regards to deal value since 2007,[1] as seen in exhibit 1. A strong Q3 and Q4 helped in reaching this point, and indicates a strong 2017. Additionally, because the strong quarters came in a time of extreme global political uncertainty surrounding events like Brexit and the U.S. presidential elections, we can be hopeful for similar reactions during the similarly uncertain year that 2017 is poised to become. Additionally, stock prices are high and interest rates are extremely low, [2] making for a favorable environment for deals.Exhibit 1

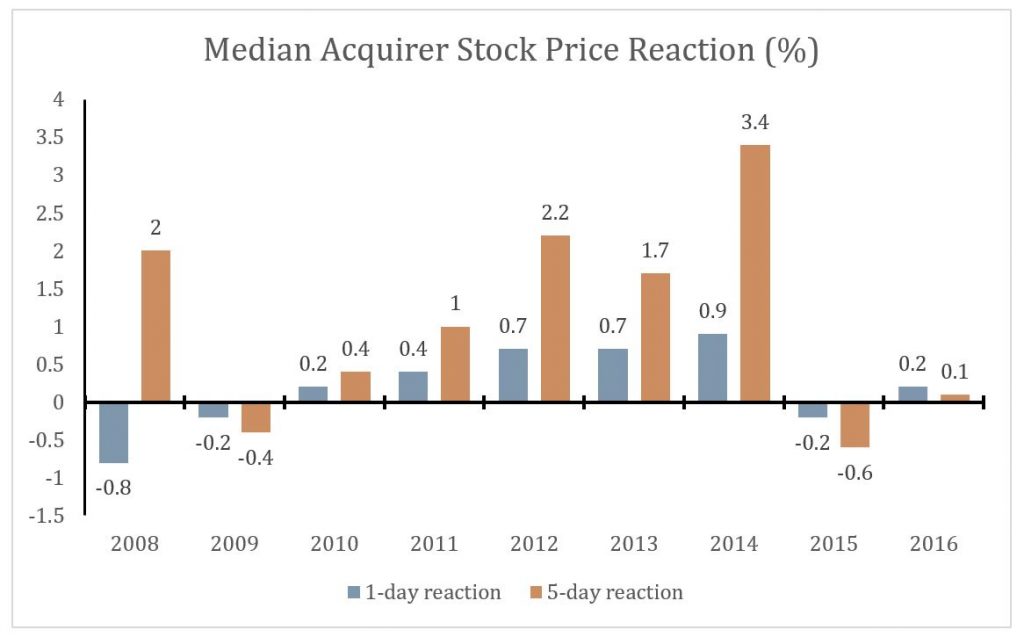

Regulatory uncertainty may turn out to boost M&A activity in 2017.[3] Donald Trump is expected to make substantial changes during his presidency, many of which could be pro-business. Lowering the corporate tax rate, reduction in regulation and cash repatriation should all provide significant opportunities for M&A through excess capital. However, it is also important to consider the adverse effects regulatory uncertainty could bring. Such uncertainty may cause complex deals to have an extended completion time causing businesses to be reluctant to pursue such deals.Market reception of significant deals is also a good sign for 2017.� In 2015, the price reaction to significant deals was negative (0.2% for one-day and 0.6% for five-day). However, 2016 yielded price reactions much closer to neutral (+0.2% for one-day and -0.1% for five-day) indicating that investors are receptive to deals.[4]

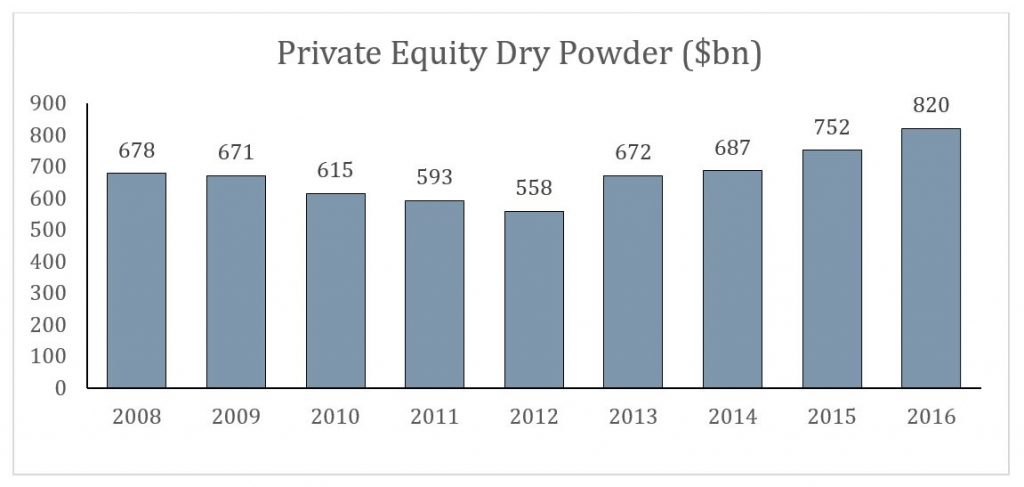

Private equity firms currently hold $822 billion in �dry powder,� or liquid assets available.� This is the most amount of dry powder held by private equity firms in the past ten years. Private equity firms should look to utilize this capital, and will provide competition to corporate buyers. PE firms will be willing to pay higher transaction multiples and expend more equity to secure a deal. This increased competition should force other buyers to do the same, raising the overall value for deals.

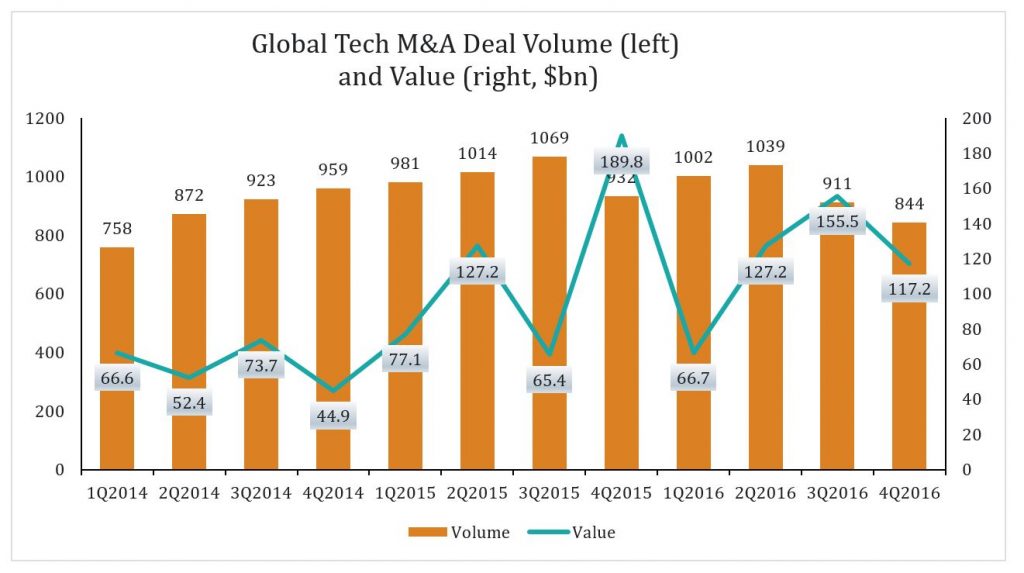

Technology to be active -Looking at exhibit 2, we can see that 3Q2016 and 4Q2016 were consecutive quarters in which total number of deals dropped. This may be concerning, but it is important to remember that 2016 set a record in terms of value for tech M&A with $466.6 billion. A drop off from a record year is expected, but the technology sector looks to remain very strong in 2017.[5]Exhibit 2

Major technology companies are carrying a high volume of cash.� Apple, Microsoft, Alphabet, Oracle and Cisco combined to hold $504 billion of the $1.7 trillion in cash and cash equivalents held by U.S. non-financial companies.[6] These high-profile technology companies are well-stocked for making major M&A moves in 2017.Non-tech companies --are becoming much more active in M&A amidst a digital transformation. In 3Q2016, 35% of companies making purchases in tech M&A were non-tech companies.[7] One example is Walmart�s $3.3 billion deal for Jet.com to aid in the transition from brick and mortar sales to ecommerce. Automobile companies are also active players in tech M&A, routinely targeting the Internet of Things to further advance their connected cars projects. This creates more competition for traditional tech companies, indicating a possible increase in average deal value in 2017.-One of the main technologies being pursued is the Internet of Things, which saw its value triple to $103.4 billion in 2016. [8]-Cybersecurity, which rose 48% to $39.8 billion in 2016, is also a very popular technology for non-tech companies. [9]-70 deals in 2016 were focused on AI and machine learning. These are two rapidly emerging technologies which could further push tech M&A activity in 2017. [10]Sources:�[1] 2016 Global M&A Report Press Release,�Mergermarket�(2017), http://mergermarket.com/info/research/2016-global-ma-report-press-release (last visited Apr 17, 2017).[2] 2017 M&A Global Outlook,�2017 M&A Global Outlook | J.P. Morgan�(2017), http://www.jpmorgan.co.kr/country/KR/en/cib/investment-banking/2017-ma-global-outlook?source=2017-ma-global-outlook_Mosaic_HomePg (last visited Apr 17, 2017).[3] 2017 M&A Global Outlook,�2017 M&A Global Outlook | J.P. Morgan�(2017)[4] 2017 M&A Global Outlook,�2017 M&A Global Outlook | J.P. Morgan�(2017)[5] EY - Technology mergers and acquisitions reports,�EY - Technology mergers and acquisitions reports - EY - Global, http://www.ey.com/gl/en/industries/technology/ey-technology-mergers-acquisitions-reports (last visited Apr 17, 2017).[6] Financial Times,�Subscribe to read, https://www.ft.com/content/368ef430-1e24-11e6-a7bc-ee846770ec15 (last visited Apr 17, 2017).[7] Joe McKendrick,�With An Eye On IoT, Non-Tech Companies Scarf Up Tech ProvidersForbes�(2016), https://www.forbes.com/sites/joemckendrick/2016/11/29/with-an-eye-on-iot-non-tech-companies-scarf-up-tech-providers/#1a1c77b93809 (last visited Apr 17, 2017).[8] Joe McKendrick,�With An Eye On IoT, Non-Tech Companies Scarf Up Tech ProvidersForbes�(2016)[9] Joe McKendrick,�With An Eye On IoT, Non-Tech Companies Scarf Up Tech ProvidersForbes�(2016)[10] Joe McKendrick,�With An Eye On IoT, Non-Tech Companies Scarf Up Tech ProvidersForbes�(2016)

.png.png)