eSports & Gaming Video Content (GVC) -- Industry Overview

The eSports industry includes the operations of organizers, sponsors, competitors and advertisers related to eSports competitions, as well as the developers and publishers of related video game content.The Gaming Video Content (GVC) industry includes related online media platforms, competitions, advertisers, video games and sponsors of video game players who stream and upload original created content online, amass public following, and receive advertising or sponsorship benefits.The reader will find it useful to analyze the two industries in parallel because they share similar market dynamics, drivers of growth, and target audience.

Analysis of one industry will provide insight on both.

Executive Summary

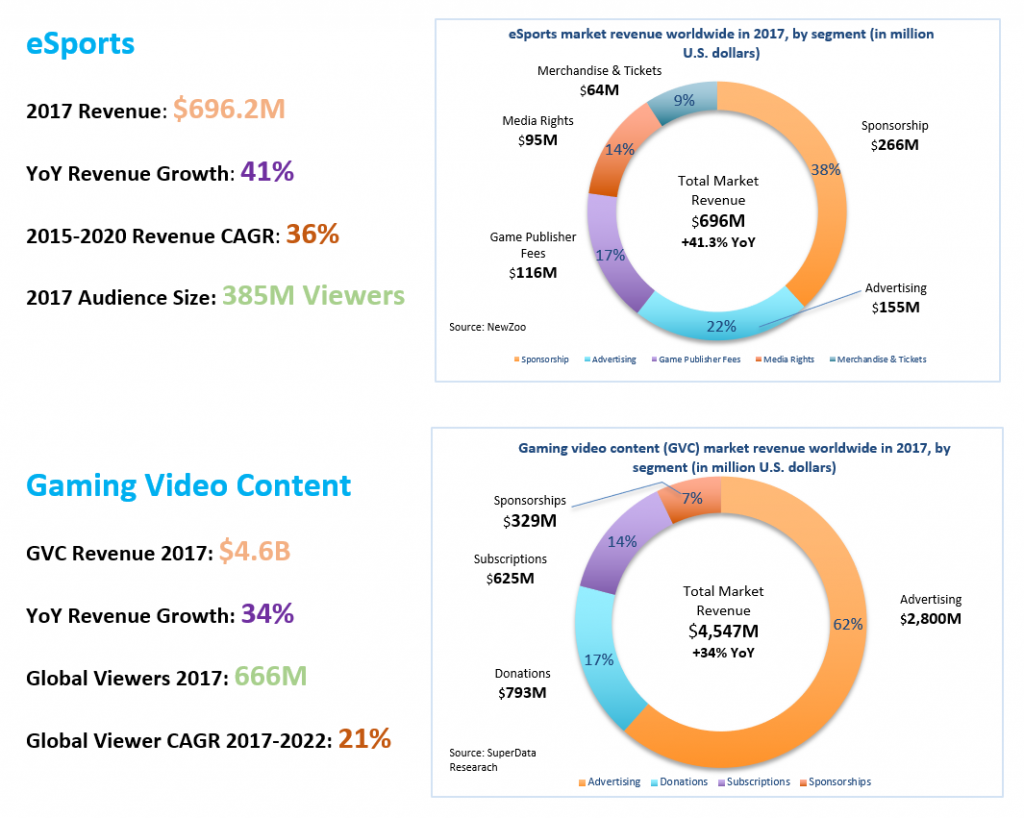

The eSports and Gaming Video Content industries have seen rapid growth in the past five yea__rs. This growth is expected to accelerate in the next five years due to several factors: the amount of viewers/subscribers of GVC and eSports will increase, more advertisers and corporate sponsors will turn to eSports and GVC to diversify their revenue, and more gamers will join professional ranks as prize pools grow.eSports is projected to have 2017 revenue of $693M and grow at a 5-year CAGR of 35.6% to $1.49B in 2020.[i] Its audience is expected to grow 20.1% CAGR from 385M viewers in 2017 to 589M viewers in 2020.[ii] The GVC industry is further along in its development, but is not yet a mature industry.

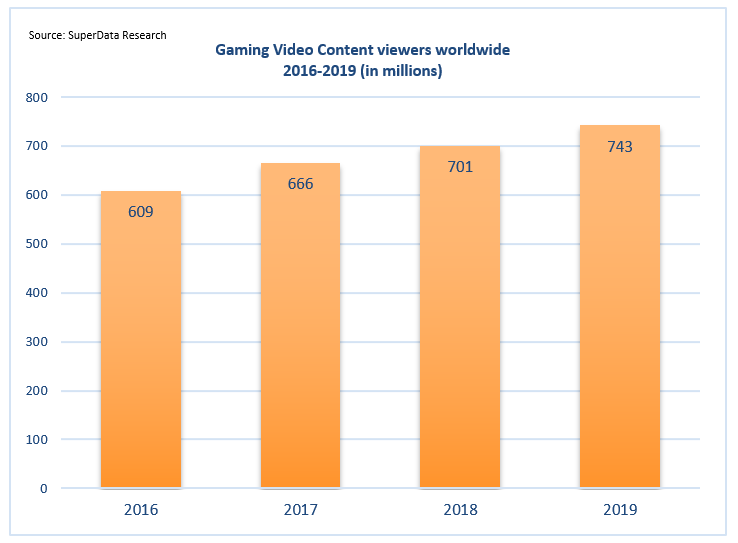

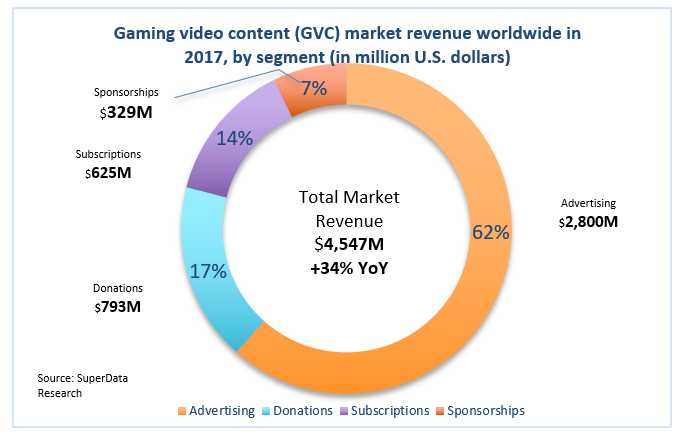

In 2017, it is expected to have a revenue of $4.6B and global audience of 666M viewers[iii]. By 2019, it’s audience is expected to be 743M.[iv] Nearly 75% of both the GVC and eSports revenue is advertising and sponsorship driven. That trend should continue as corporate sponsors and advertisers seek to tap into the loyal, millennial demographic that constitutes the majority of the online gaming ecosystem.The eSports market is still highly fragmented as teams and leagues continue to surface and solidify their system and revenue models.

The GVC market is more stable with two main competitors, Amazon-owned Twitch and Google-owned YouTube Gaming, dominating the market. The main risk associated with both markets is the lack of profitability as leagues, teams, and sponsors develop their revenue models. The main barrier to entry is the intensifying competition for top players and teams in the best leagues. Investment groups from other traditional sports have already begun to invest millions of dollars in teams to capture the upside of the expected growth.

Key Drivers & Trends

- The Behavioral Trend: People are willing to pay to watch other people play video games —

In 2016, 609M people worldwide spent over 5B hours watching video game streams of some kind on the internet.[v][vi] This statistic alone highlights the most significant driver of the massive industry growth: people enjoy watching other people play video games, and are willing to pay to have a quality experience. Most GVC viewers and eSports enthusiasts are millennials, and most have a full-time job and earn mid to high income.[vii] As the Millennial generation — the generation that grew up with video games as its primary source of entertainment — grows older, they are seeking to watch their favorite pastime instead of play it.

GVC platforms Twitch and YouTube Gaming accounted for 702M viewers in 2016 — more viewers than HBO, Netflix, Spotify, ESPN, and Hulu combined.[viii] This highlights the trend that more consumers are choosing GVC and eSports as their primary source of entertainment.—

- eSports and GVC represent a new, untapped revenue source —

For years corporate brands have sought access to the growing amount of hours young people spend playing video games. The growth, stability, and accessibility of eSports leagues and GVC media outlets represents such an opportunity. Of the estimated $696M of global market revenue that eSports is projected to generate, 74% or $516.8M will come from sponsorship, advertising, and media rights fees, with some sources saying that number is upwards of $660M.[ix][x] The Gaming Video Content industry boasts an estimated 2017 market revenue of $4.6B and advertising revenue stream of $2.8B.

This is due in large part to its 666M worldwide viewers in 2017.[xi] That number is projected to consistently increase at a 3 year CAGR of 21% to 743M viewers in 2019.[xii] The advertising and sponsorship revenue streams are expected to grow at a similar pace. This trend is especially evident for professional sports clubs who view eSports as an opportunity to diversify their revenue streams and capture those not previously interested in traditional sports.

Many NBA and professional soccer clubs in Europe and South America have signed professional gamers to represent their respective club in eSports competitions of every kind.[xiii][xiv][xv][xvi] The race to sign competitive gamers is expected to intensify as corporate brands hope to tap into a new revenue stream.

- Development of relatively cheap live stream capability on non-traditional platforms —

The development of technology that allows average video gamers to live stream their own content and for video game tournaments to live stream their competition has contributed to the growth of the eSports and GVC industries. Twitch and YouTube Gaming allow for relatively cheap entry for gamers to create their own live streams. The average income that gamers can make streaming content online is estimated to be between $60-75K a year, with the upper bound now pushing $4M annually.[xvii] Live stream gamers must be willing to pay for a live stream subscription as well as audio/visual equipment needed to facilitate a quality stream.

With relatively low barriers to entry and increasing incentive and demand for quality content, more gamers will continue to join the live stream gaming ecosystem.

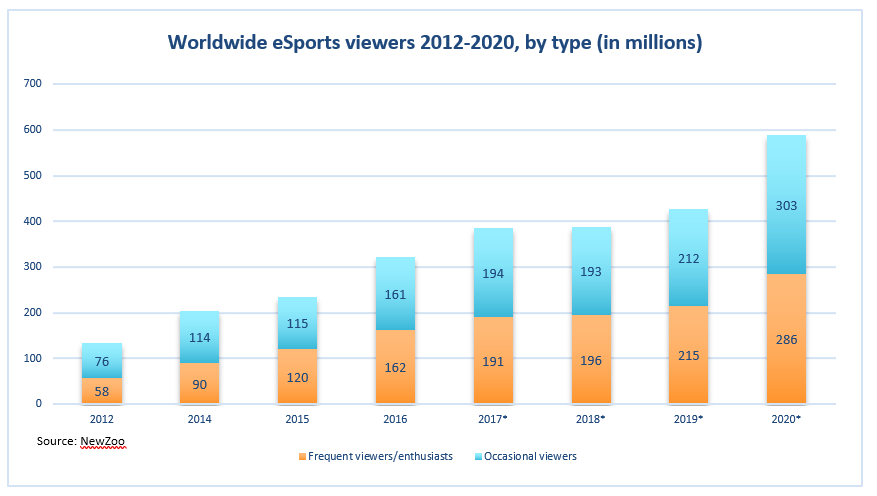

Live stream technology has also facilitated the rapid acceleration of viewership and growth of eSports leagues and competitions. This is shown in part by the growth in viewership of eSport competitions from 134M viewers in 2012 to over 385M viewers in 2017, and the growth of online streaming outlets - like Twitch - which live stream global competitions.[xviii]

Competitive Landscape

Major eSport Competitions and Leagues — Thousands of tournaments are hosted every year playing several different video games for varying prize pool sizes. There is no dominant or unified league that mandates or regulates the eSports industry. The publisher of each video game reserves the right to determine how its competitions are structured. This leads to a variety of competitive structures and revenue models.

This lack of uniformity causes some instability and uncertainty in the growing eSports market. Because of this, there has yet to be a clear leader in the video game publishing realm, and the eSports and GVC markets remain relatively fragmented due to the variety of games and competitions in the gaming ecosystem.

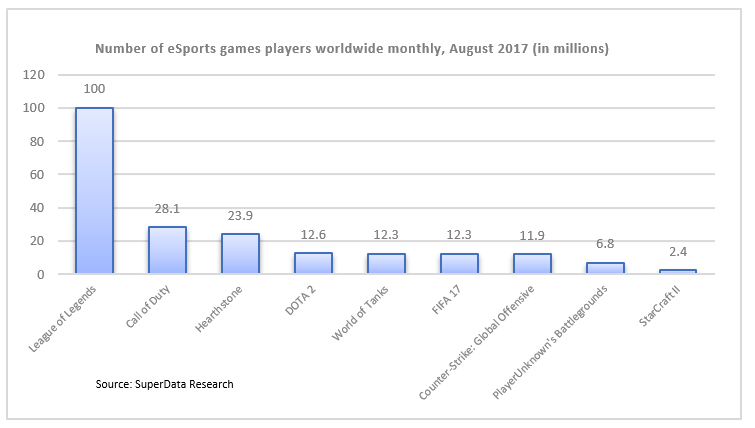

Major Games “With more than 100 games used in professional competitions, the competition to gain market share is high and the market is fragmented. The most played games in competition are highly dependent on factors such as the game’s broader casual fan base, fans” interest level in watching, price point to buy game and enter competitions, and the publisher/developer’s involvement in the competition. League of Legends is considered to be the market leader with over 100M active monthly competitors.[xix]

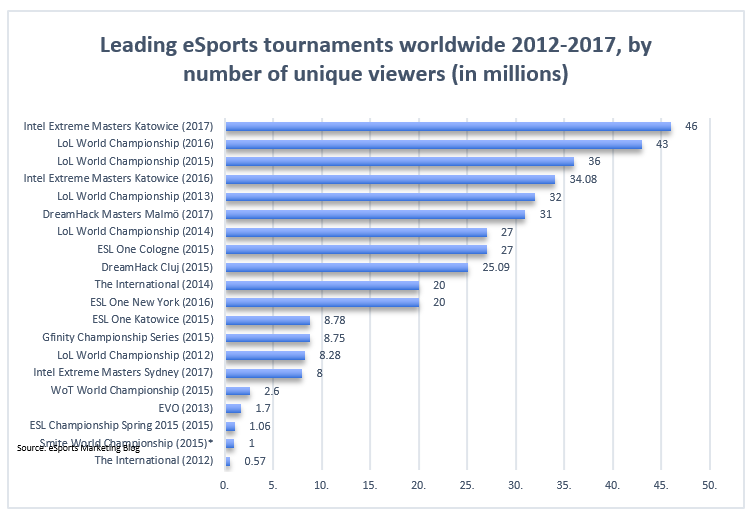

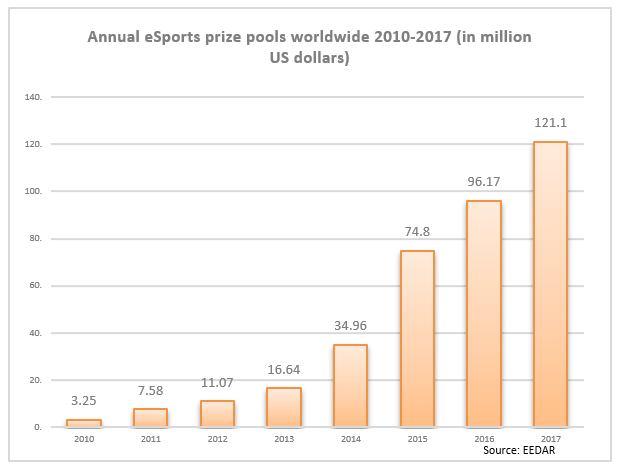

For of the past ten years, the record for largest prize pools and highest amount of unique tournament viewers has surpassed previous records demonstrating rapid growth. Dota 2, a direct competitor of LoL, consistently draws the largest prize pools. The 2017 Dota International amassed a record prize pool of $24.69M, with $2.16M going to each of the five members of the winning team.[xx] That sum is on par with the winning purse of many established sport tournaments.[xxi] The 2017 IEM attracted an eSports all-time record 46M unique viewers, 3M more than the 2016 LoL World Championships, 5.5M more than the Game 7 of the 2016 World Series, and 15M more than Game 7 of the 2016 NBA finals.[xxii][xxiii][xxiv]

The online streaming market is dominated by Amazon’s Twitch and Google’s YouTube Gaming. Twitch is one of the world’s leading video service platforms. Bought by Amazon in 2014 for $970M, Twitch attracts 15M active users daily and more than 2.2M unique content creators monthly.[xxv] Although its content includes music and creative arts, Twitch has emerged as the leading platform in the world for streaming video game content.

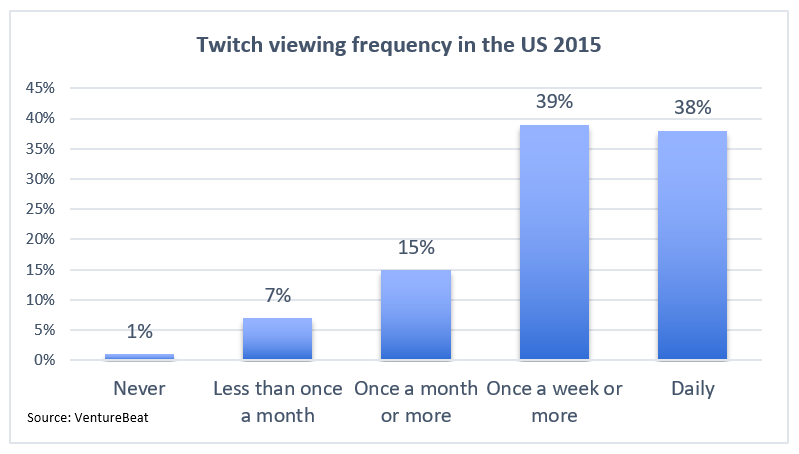

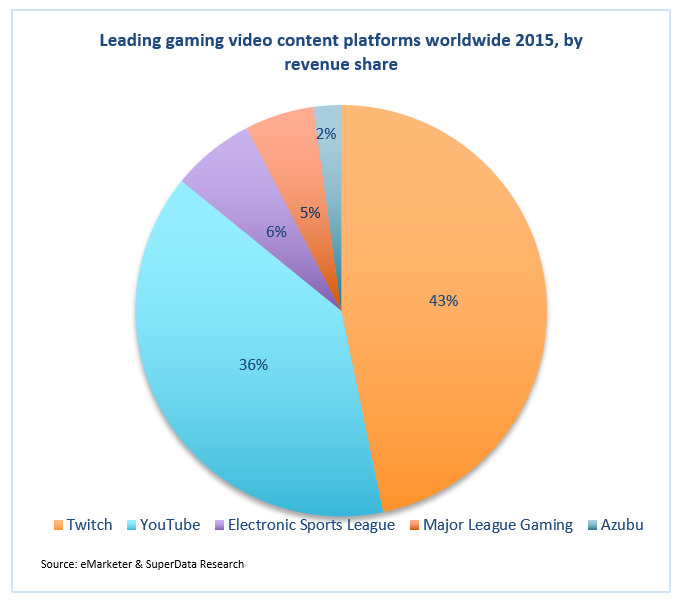

In 2016, Twitch had over 185M viewers of Gaming Video Content.[xxvi] Twitch has an extremely loyal fan base with 38% of US Twitch viewers reporting to watch content daily and an additional 39% of viewers reporting to watch content at least once a week or more.[xxvii] As of 2015, Twitch earns 43% of all market revenue despite only carrying 16% of its viewers, 7% more than its closest competitor, Google’s YouTube Gaming.[xxviii][xxix] This is due in part to Amazon recently adding the ability for viewers to purchase PC games and game add-ons directly from Twitch in order to capture viewers’ willingness to spend.

YouTube Gaming is the gaming subsite of YouTube which allows users to live stream, upload, and playback gaming video content. It launched in August 2015 to compete with Amazon’s Twitch. Although years behind Twitch in audience development, YouTube Gaming quickly caught up because of its massive pre-existing user base. Since its inception in 2015, gaming has become the second largest category on YouTube after music with nearly 77M subscribers.[xxx] In 2016, YouTube registered over 517M viewers of GVC, almost 3x as many as Twitch over the same time period.[xxxi] Despite its large user base and clear advantage in overall viewers, YouTube Gaming has yet to monetize its subscribers as adeptly as Twitch claiming only 36% of market revenue to Twitch’s 43%.[xxxii] YouTube’s traditional strength of playback of recorded videos and Twitch’s emphasis on live streams is evident in the most recent numbers.

In the Q2 2017, Twitch averaged more than 6K more live streamers and over 400K more live stream viewers than YouTube.[xxxiii][xxxiv] This highlights the hierarchy of viewer choice: Twitch is the preferred platform for gamers to watch live content, most likely due to its partnership with major eSports organizations.

Audience

Demographic — The eSports and GVC audience is a highly sought after demographic in terms of advertising and investment. The audience skews young and male with more than half falling in the male, 21-35 year old age bucket.[xxxv] They consume the majority of content online in lieu of traditional outlets. The percentage make up of millennials in the GVC and eSports audience is two to three times higher than any of the big four sports.[xxxvi] Historically millennials have been among the hardest demographics to reach via traditional media, so this audience make up suggests large opportunity for future advertising and broadcast rights sales.Willingness to Spend — Most GVC viewers and eSports enthusiasts have a full-time job and enjoy mid to high income.[xxxvii].

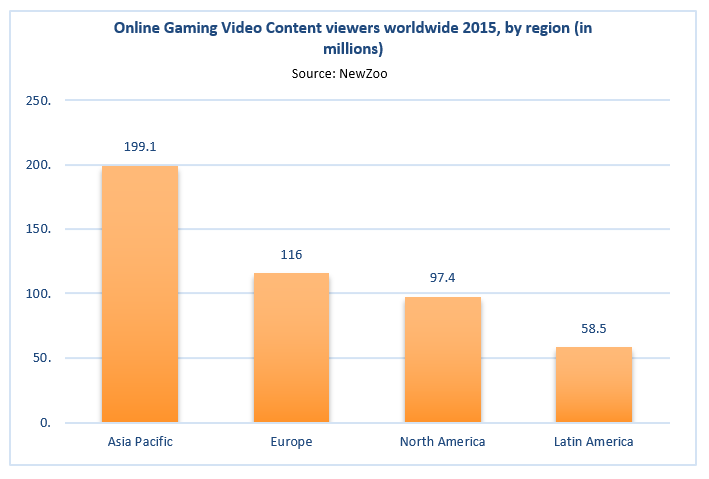

GVC viewers are highly loyal to the streamers they follow and are willing to pay to have access to ad-free streams or to earn on-air shout outs.[xxxviii]Geography — The Asia Pacific region represents the highest portion of eSports and GVC enthusiasts. China accounts for more than half of the global eSports audience. The Chinese accounted for 57% of all viewing last year and watched eSports broadcasts more than 11 billion times — four times as often as eSports' second-largest market, North America.—The Asia Pacific region also takes first place in GVC viewers.[xxxix] As of 2015, Asia Pacific accounted for 199.1M viewers, 83M more than Europe, and 102M more than North America.[xl]

Barriers to Entry & Market Risks

Lack of profitability — The greatest challenge to the world of eSports and GVC is turning a profit. Despite year over year revenue increases, becoming profitable is viewed by most experts as years away for two main reasons. Because eSports is such a young industry, almost all left over cashflow is reinvested to bolster league and team growth for the future. And publishers, teams, and advertisers are all still trying to solidify their revenue models.

This represents the primary risk of the current eSports world — lack of a profitable revenue model. Questions regarding open vs. closed circuit competitions, salaries vs. large prize pools, how to fund prize pools, and how to structure player contracts have yet to be answered. From an investor perspective, as more money from advertisers and sponsors funnels into the industry, volatility appears to decrease.

But most investors are still unsure how and when ROI will come.Competition — Despite being in its infancy, both the GVC and eSports industries have rapidly become very competitive markets. eSports teams must attract the best players with more benefits and prospective success. Twitch and YouTube have a near stranglehold on the streaming industry. Riot and Valve, publishers of LoL and Dota 2 respectively, represent a significant hold on the gaming market because of their loyal fan bases.

With money from advertisers, sponsors, and investors increasing, competition to join the gaming world will intensify and presents a significant barrier to entry for potential market participants.[i]2017 Global Esports Market Report, www.newzoo.com (2017), http://resources.newzoo.com/hubfs/Reports/Newzoo_Free_2017_Global_Esports_Market_Report.pdf?hsCtaTracking=5a96aa39-a810-47a6-834b-559c317775c3%7C6a2d5758-bab2-4d87-9fbe-f82dc9ba638a (last visited Nov 2, 2017).[ii]2017 Global Esports Market Report, www.newzoo.com (2017), http://resources.newzoo.com/hubfs/Reports/Newzoo_Free_2017_Global_Esports_Market_Report.pdf?hsCtaTracking=5a96aa39-a810-47a6-834b-559c317775c3%7C6a2d5758-bab2-4d87-9fbe-f82dc9ba638a (last visited Nov 2, 2017).[iii] SuperData Research, Gaming video content (GVC) market revenue worldwide in 2017, by segment (in million U.S. dollars), Statista, https://www-statista-com.erl.lib.byu.edu/statistics/761204/gaming-video-content-revenue/ (last visited Nov.

5, 2017).[iv] SuperData Research, Number of gaming video content (GVC) viewers worldwide from 2016 to 2019 (in millions), Statista, https://www-statista-com.erl.lib.byu.edu/statistics/516754/gaming-video-content-viewer-number-global/ (last visited Nov. 5, 2017).[v] SuperData Research, Number of gaming video content (GVC) viewers worldwide from 2016 to 2019 (in millions), Statista, https://www-statista-com.erl.lib.byu.edu/statistics/516754/gaming-video-content-viewer-number-global/ (last visited Nov.

5, 2017).[vi] Caitlin Dewey, The Internet spent a whopping 2.4 billion hours watching “competitive video games” last year The Washington Post (2014), https://www.washingtonpost.com/news/the-intersect/wp/2014/06/03/the-internet-spent-a-whopping-2-4-billion-hours-watching-competitive-video-games-last-year/?utm_term=.1555a13f7d3e%29 (last visited Nov 5, 2017).[vii] 2017 Global Esports Market Report, www.newzoo.com (2017), http://resources.newzoo.com/hubfs/Reports/Newzoo_Free_2017_Global_Esports_Market_Report.pdf?hsCtaTracking=5a96aa39-a810-47a6-834b-559c317775c3%7C6a2d5758-bab2-4d87-9fbe-f82dc9ba638a (last visited Nov 2, 2017).[viii]Gaming videos are bigger than HBO, Netflix, and Hulu combined, PCGamesN (2017), https://www.pcgamesn.com/twitch-youtube-netflix-subscribers (last visited Nov 4, 2017).[ix] Esports Revenues Deep Dive: The Esports Economy Is Expanding Rapidly but ROI Is Still Limited, Newzoo (2017), https://newzoo.com/insights/articles/esports-revenues-deep-dive-the-esports-economy-is-expanding-rapidly-but-roi-is-still-limited-for-most-individual-companies/ (last visited Nov 7, 2017).[x] SuperData Research, eSports market revenue worldwide in 2016, by segment (in million U.S. dollars), Statista, https://www-statista-com.erl.lib.byu.edu/statistics/490358/esports-revenue-worldwide-by-segment/ (last visited Nov.

7, 2017).[xi] SuperData Research, Gaming video content (GVC) market revenue worldwide in 2017, by segment (in million U.S. dollars), Statista, https://www-statista-com.erl.lib.byu.edu/statistics/761204/gaming-video-content-revenue/ (last visited Nov. 5, 2017).[xii] SuperData Research, Number of gaming video content (GVC) viewers worldwide from 2016 to 2019 (in millions), Statista, https://www-statista-com.erl.lib.byu.edu/statistics/516754/gaming-video-content-viewer-number-global/ (last visited Nov.

5, 2017).[xiii] Mike Kent, Full List Of Professional Sports Teams In Esports | Esports News & Videos Dexerto (2016), https://www.dexerto.com/news/full-list-of-professional-sports-teams-in-esports/19056 (last visited Nov 5, 2017).[xiv] 2017 Global Esports Market Report, www.newzoo.com (2017), http://resources.newzoo.com/hubfs/Reports/Newzoo_Free_2017_Global_Esports_Market_Report.pdf?hsCtaTracking=5a96aa39-a810-47a6-834b-559c317775c3%7C6a2d5758-bab2-4d87-9fbe-f82dc9ba638a (last visited Nov 2, 2017).[xv] Zach Lowe,—NBA, Take-Two Interactive Software partnering on NBA 2K esports league ESPN(2017), http://www.espn.com/nba/story/_/id/18647863/nba-take-two-interactive-software-partnering-nba-2k-esports-league (last visited Nov 3, 2017).[xvi] Jacob Wolf,—The NBA and esports: How we got here ESPN—(2017), http://www.espn.com/esports/story/_/id/18702213/the-nba-esports-how-got-here (last visited Nov 5, 2017).[xvii] How Much Money Do Video Game Streamers Really Make?

A Look At Twitch's Top Earners, How Much Money Do Streamers Make? A Look At Twitch's Top Earners (2017), https://nowloading.co/p/how-much-money-video-game-streamers-make/4266946 (last visited Nov 7, 2017).[xviii] Newzoo, eSports audience size worldwide from 2012 to 2020, by type of viewers (in millions), Statista, https://www-statista-com.erl.lib.byu.edu/statistics/490480/global-esports-audience-size-viewer-type/ (last visited Nov.

5, 2017).[xix] SuperData Research, Number of players of selected eSports games worldwide as of August 2017 (in million), Statista, https://www-statista-com.erl.lib.byu.edu/statistics/506923/esports-games-number-players-global/ (last visited Nov. 8, 2017).[xx] The International 2017: Dota 2 Championships - Tournament Results & Prize Money, e-Sports Earnings, https://www.esportsearnings.com/tournaments/24181-the-international-2017 (last visited Nov 6, 2017).[xxi] Oliver Cragg,—How does record-breaking Dota 2 TI6 prize money compare to major sporting competitions?—International Business Times UK—(2016), http://www.ibtimes.co.uk/dota-2-international-how-does-esports-record-prize-compare-major-sporting-competitions-1573071 (last visited Nov 5, 2017).[xxii] John Koblin,—Game 7 of N.B.A.

Finals Draws Close to 31 Million Viewers The New York Times(2016), https://www.nytimes.com/2016/06/21/business/media/game-7-of-nba-finals-draws-close-to-31-million-viewers.html?smid=tw-nytimes&smtyp=cur (last visited Nov 6, 2017).[xxiii] UPDATED: SHOWBUZZDAILY’s Top 150 Wednesday Cable Originals—& Network Finals: 11.2.2016,—Showbuzz Daily, http://www.showbuzzdaily.com/articles/showbuzzdailys-top-150-wednesday-cable-originals-network-finals-11-2-2016.html (last visited Nov 6, 2017).[xxiv] eSports Marketing Blog, Number of unique viewers of selected eSports tournaments worldwide from 2012 to 2017 (in millions), Statista, https://www-statista-com.erl.lib.byu.edu/statistics/507491/esports-tournaments-by-number-viewers-global/ (last visited Nov.

7, 2017).[xxv] Craig Smith,—46 Amazing Twitch Stats and Facts DMR—(2017), https://expandedramblings.com/index.php/twitch-stats/ (last visited Nov 5, 2017).[xxvi] Report Launch: Gaming Video Content is bigger than streaming and sports networks, www.superdataresearch.com (2017), https://www.superdataresearch.com/report-launch-gaming-video-content-is-bigger-than-streaming-and-sports-networks/ (last visited Nov 4, 2017).[xxvii] VentureBeat, Frequency of viewing Twitch according to Twitch viewers in the United States in 2015, Statista, https://www-statista-com.erl.lib.byu.edu/statistics/532338/twitch-viewing-frequency-usa/ (last visited Nov.

7, 2017).[xxviii] eMarketer & SuperData Research, Leading platforms for viewing gaming video content worldwide as of May 2015, by revenue share, Statista, https://www-statista-com.erl.lib.byu.edu/statistics/446060/gaming-video-content-platforms-revenue-share/ (last visited Nov. 5, 2017).[xxix] Report Launch: Gaming Video Content is bigger than streaming and sports networks, www.superdataresearch.com (2017), https://www.superdataresearch.com/report-launch-gaming-video-content-is-bigger-than-streaming-and-sports-networks/ (last visited Nov 4, 2017).[xxx] Report Launch: Gaming Video Content is bigger than streaming and sports networks, www.superdataresearch.com (2017), https://www.superdataresearch.com/report-launch-gaming-video-content-is-bigger-than-streaming-and-sports-networks/ (last visited Nov 4, 2017).[xxxi] Report Launch: Gaming Video Content is bigger than streaming and sports networks, www.superdataresearch.com (2017), https://www.superdataresearch.com/report-launch-gaming-video-content-is-bigger-than-streaming-and-sports-networks/ (last visited Nov 4, 2017).[xxxii] eMarketer & SuperData Research, Leading platforms for viewing gaming video content worldwide as of May 2015, by revenue share, Statista, https://www-statista-com.erl.lib.byu.edu/statistics/446060/gaming-video-content-platforms-revenue-share/ (last visited Nov.

5, 2017).[xxxiii] Streamlabs, Average number of streamers on YouTube Gaming Live and Twitch in 2nd quarter 2017, Statista, https://www-statista-com.erl.lib.byu.edu/statistics/761100/average-number-streamers-on-youtube-gaming-live-and-twitch/ (last visited Nov. 7, 2017).[xxxiv] Streamlabs, Average number of viewers on YouTube Gaming Live and Twitch in 2nd quarter 2017, Statista, https://www-statista-com.erl.lib.byu.edu/statistics/761122/average-number-viewers-on-youtube-gaming-live-and-twitch/ (last visited Nov.

7, 2017).[xxxv] 2017 Global Esports Market Report, www.newzoo.com (2017), http://resources.newzoo.com/hubfs/Reports/Newzoo_Free_2017_Global_Esports_Market_Report.pdf?hsCtaTracking=5a96aa39-a810-47a6-834b-559c317775c3%7C6a2d5758-bab2-4d87-9fbe-f82dc9ba638a (last visited Nov 2, 2017).[xxxvi] Robert Elder,—Esports is far from fulfilling its revenue potential, but growing steadily Business Insider—(2017), http://www.businessinsider.com/esports-is-nascent-but-growing-steadily-2017-5 (last visited Nov 2, 2017).[xxxvii] 2017 Global Esports Market Report, www.newzoo.com (2017), http://resources.newzoo.com/hubfs/Reports/Newzoo_Free_2017_Global_Esports_Market_Report.pdf?hsCtaTracking=5a96aa39-a810-47a6-834b-559c317775c3%7C6a2d5758-bab2-4d87-9fbe-f82dc9ba638a (last visited Nov 2, 2017).[xxxviii] Report Launch: Gaming Video Content is bigger than streaming and sports networks, www.superdataresearch.com (2017), https://www.superdataresearch.com/report-launch-gaming-video-content-is-bigger-than-streaming-and-sports-networks/ (last visited Nov 4, 2017).[xxxix] Robert Elder,—Esports is far from fulfilling its revenue potential, but growing steadily Business Insider—(2017), http://www.businessinsider.com/esports-is-nascent-but-growing-steadily-2017-5 (last visited Nov 2, 2017).[xl]Newzoo, Number of online gaming video content viewers worldwide in 2015, by region (in millions), Statista, https://www-statista-com.erl.lib.byu.edu/statistics/516776/gaming-video-content-viewer-number-global-region/ (last visited Nov.

5, 2017).Contributors to this article:William Montgomery

Considering a transaction?

Speak with our advisory team about your sell-side, buy-side, or capital needs — in confidence.