This is the sixth in a multi-part series that will focus on the major companies and activity in the medical device manufacturing industry, a member of the manufacturing sector.

Major Companies

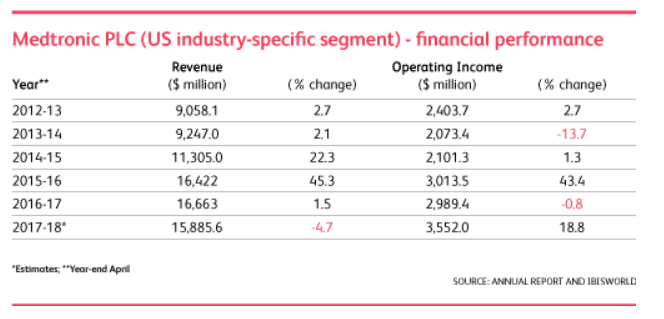

[1] Medtronic PLC Medtronic develops and manufactures medical devices for chronic diseases and commands 40.2% of the market share. It sells its products in over 140 countries worldwide. Foreign sales account for 40% of the company’s total revenue. It employs about 45,000 people. It’s four largest segments are cardiac and vascular (46.2%), restorative therapies (33.3%), minimally invasive technologies (11.8%), and diabetes management products (8.7%).

Medtronic has focused on acquisition to broaden the scope of products it offers and expand international presence. The company recently acquired medical supplies giant Covidien for $42.9 billion and is shifting its headquarters to Dublin to save in US taxes. The company is able to maintain low revenue volatility due to its diversified product mix.

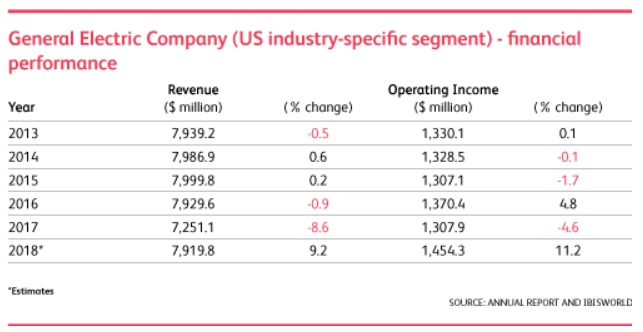

[1] General Electric General Electric has roughly 20% market-share and employs more than 300,000 people across the globe. Its medical device manufacturing division represents roughly 16% of its total revenue. In recent years it has acquired API Healthcare and some of Thermo Fisher Scientific. The majority of GE’s business is outside the United States and it has continued expanding its presence in emerging markets.

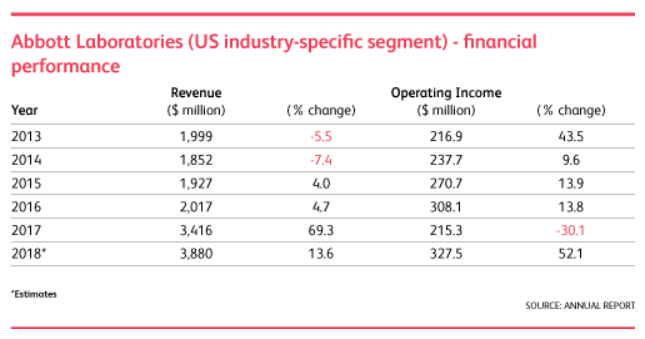

[1] Abbott Laboratories Abbott Laboratories is the third largest presence in this space with 9.8% market share. It manufactures about 31% of its products in the United States. Its acquisition of St. Jude Medical Inc. in 2017 transformed it into a dominant industry player. Its profit is expected to grow 52% in 2018 in large part to its acquisition of St. Jude Medical Inc.

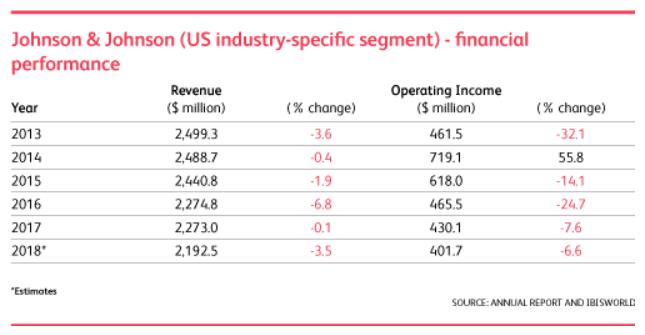

[1] Johnson & Johnson Johnson & Johnson is a family name and leading healthcare company globally. They currently hold 5.5% market share and estimate 2018 industry-specific revenue will total $2.2 billion. It operates primarily in the United States and Europe though is rapidly expanding in Asia. It attributes demand for cardiovascular products for growing sales.

[1] Other notable firms are Boston Scientific Corporation (4–5% market share), Danaher Corporation (4–5% market share), and Varian Medical Systems Inc (1–2% market share).

Primary Activity

The medical device manufacturing industry (U.S. only) experienced its largest year in deals, by count, in 2016. When it comes to the type of deal, Buyout and Leveraged Buyouts (LBOs) are the most common.

Recent large deals include:

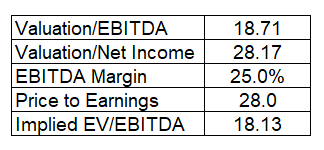

1. Medtronic’s acquisition of Covidien completed in January 2015 for $42.9 billion. Important deal multiples are as follows:

[2] 2. Johnson & Johnson’s acquisition of Abbott Medical Optics completed in February 2017 for $4.3 billion. This strategic acquisition will help Johnson & Johnson expand their eye care portfolio.

3. In December 2017 Becton, Dickinson and Company announced the completion of their acquisition of C.R. Bard. The acquisition is expected to create a company with approximately $16 billion in annualized revenue. C.R. Bard shareholders received $222.93 in cash and 0.5077 of a share of Becton Dickinson common stock for each outstanding share. [3]

What Drives M&A Activity in Medical Device Manufacturing?

The medical device sector’s sustained M&A activity reflects structural dynamics that have persisted across market cycles. Understanding these drivers helps practitioners contextualize both the strategic logic behind major transactions and the valuation frameworks applied to smaller, privately held device companies.

Regulatory pathway optimization. FDA clearance and approval timelines represent significant capital and time investments. Acquiring a company that has already secured clearance for a complementary product—or that has an established quality management system—can accelerate time-to-market for the acquirer’s pipeline products far more efficiently than internal development.

Geographic expansion efficiency. Medical device distribution is heavily relationship-dependent. Acquiring established regional or international distributors and manufacturers provides immediate access to hospital purchasing networks, GPO relationships, and reimbursement codes that would take years to build organically. This pattern is visible in GE’s continued emerging market expansion and in Medtronic’s Dublin repositioning.

Platform consolidation. Larger strategics pursue bolt-on acquisitions to build comprehensive product platforms that allow hospitals to standardize on a single vendor across multiple care categories. This consolidation dynamic creates acquisition demand for smaller, specialized device companies with defensible niches and strong clinical outcomes data.

For a more detailed analysis of transaction structures, valuation benchmarks, and deal activity trends in this sector, the companion piece on medical device M&A trends and valuation provides additional context.

Valuation Considerations for Medical Device Companies

Valuing a medical device business requires understanding which metrics buyers and investors weight most heavily. Unlike many manufacturing businesses, device companies are often valued on forward revenue multiples or pipeline value rather than trailing EBITDA alone—particularly when significant regulatory milestones or reimbursement events lie ahead.

Key value drivers typically include:

- Revenue mix and recurring characteristics: Consumables, disposables, and service contracts attached to capital equipment generate more predictable cash flows than one-time capital placements, and are generally valued at higher multiples.

- FDA clearance status: 510(k)-cleared products with established reimbursement codes carry lower regulatory risk than pre-market approval products still in clinical trials.

- Customer concentration: Heavy dependence on a small number of hospital systems or GPO contracts introduces risk that buyers will price into their offers.

- IP and patent position: Defensible intellectual property creates barriers to competitive entry and supports premium multiples, particularly for acquirers seeking to lock in a technology advantage.

Owners of medical device companies exploring a sale or recapitalization should review detailed transaction comparables specific to their product category and revenue profile. The broader context of medical device transaction activity provides deal-level data that supports more informed valuation benchmarking.

The Role of Due Diligence in Device Company Transactions

Medical device M&A transactions involve diligence workstreams that extend well beyond standard financial and legal review. Buyers conduct regulatory diligence—including review of complaint files, MDR (Medical Device Report) submissions, FDA inspection history, and quality system audit records—to assess whether the target’s compliance posture will withstand post-close scrutiny.

Quality system deficiencies identified during diligence can become transaction-breaking issues or result in significant price adjustments. Sellers who invest in quality system remediation before entering a formal process—and who can present clean inspection histories—reduce the discount that buyers apply for perceived regulatory risk. Structuring and organizing these materials through a data room workflow purpose-built for transaction diligence improves the efficiency of the buyer review process and signals organizational sophistication.

Owners considering a transaction in the near term can benefit from beginning the preparation process early. Preparing a transaction with appropriate lead time allows quality, regulatory, and financial issues to be addressed before they surface in buyer diligence—rather than in the middle of a negotiation when leverage is lowest.

Mohammed Siddiqui contributed to this report.

Sources

[1] Medical Device Manufacturing in the US (Industry Report 33451b). Retrieved August 2, 2018, from IBISWorld database.

[2] PitchBook data found searching the following keywords: “medical device manufacturer.”

[3] Becton, Dickinson and Company. (2017, December 29). BD Completes Bard Acquisition, Creating New Global Health Care Leader. Retrieved August 9, 2018, from http://www.bd.com/en-us/company/news-and-media/press-releases/dec-29-2017-bd-completes-bard-acquisition-creating-new-global-health-care-leader.

Frequently Asked Questions

What types of buyers are most active in medical device M&A?

Both strategic acquirers (large device OEMs seeking to expand product portfolios) and financial buyers (private equity firms building platform companies through consolidation) are active in this space. Strategic buyers typically pay higher multiples when the target offers a meaningful technology, regulatory, or distribution synergy. Financial buyers are generally more return-driven and often focus on businesses with recurring revenue streams and margin expansion potential.

How are smaller, privately held medical device companies typically valued?

Smaller device companies are most commonly valued on EBITDA multiples, revenue multiples, or a blended approach depending on their growth stage. Companies with FDA-cleared products and established commercial revenue are typically valued on EBITDA; pre-revenue or early-commercial companies with significant pipeline value are more often valued on revenue or strategic value to a specific acquirer. Market comparables from transactions in similar device categories provide the most reliable benchmarking data.

What is the significance of the 510(k) clearance pathway in an M&A context?

A 510(k)-cleared product has demonstrated substantial equivalence to an existing legally marketed device, which typically means a faster, less costly regulatory pathway than a PMA (Pre-Market Approval). In M&A, 510(k) status signals lower regulatory risk because the clearance framework is well understood by buyers, their counsel, and their quality consultants. PMA products carry higher regulatory scrutiny, longer approval timelines, and post-market study obligations that can introduce diligence complexity.

How does capital intensity affect medical device company valuations?

High capital intensity—whether from manufacturing equipment, cleanroom facilities, or R&D infrastructure—can compress free cash flow multiples even when EBITDA margins appear healthy. Buyers assess whether existing capital assets are sufficient to support projected growth or whether significant additional investment will be required post-close. For a more detailed discussion of how capital intensity affects valuation in this sector, the analysis of medical device capital intensity provides a focused treatment of this topic.

Considering a transaction?

Speak with our advisory team about your sell-side, buy-side, or capital needs — in confidence.